Consumerizing the private markets

The private markets are becoming accessible to the masses. Entrepreneurs building tools and platforms that expand private market participation will shape culture and economic opportunity for decades.

The United States is celebrated as a free-market economy, yet access to one of the largest and most important asset classes—private equity & venture capital—is reserved almost exclusively for institutions and high net worth individuals.

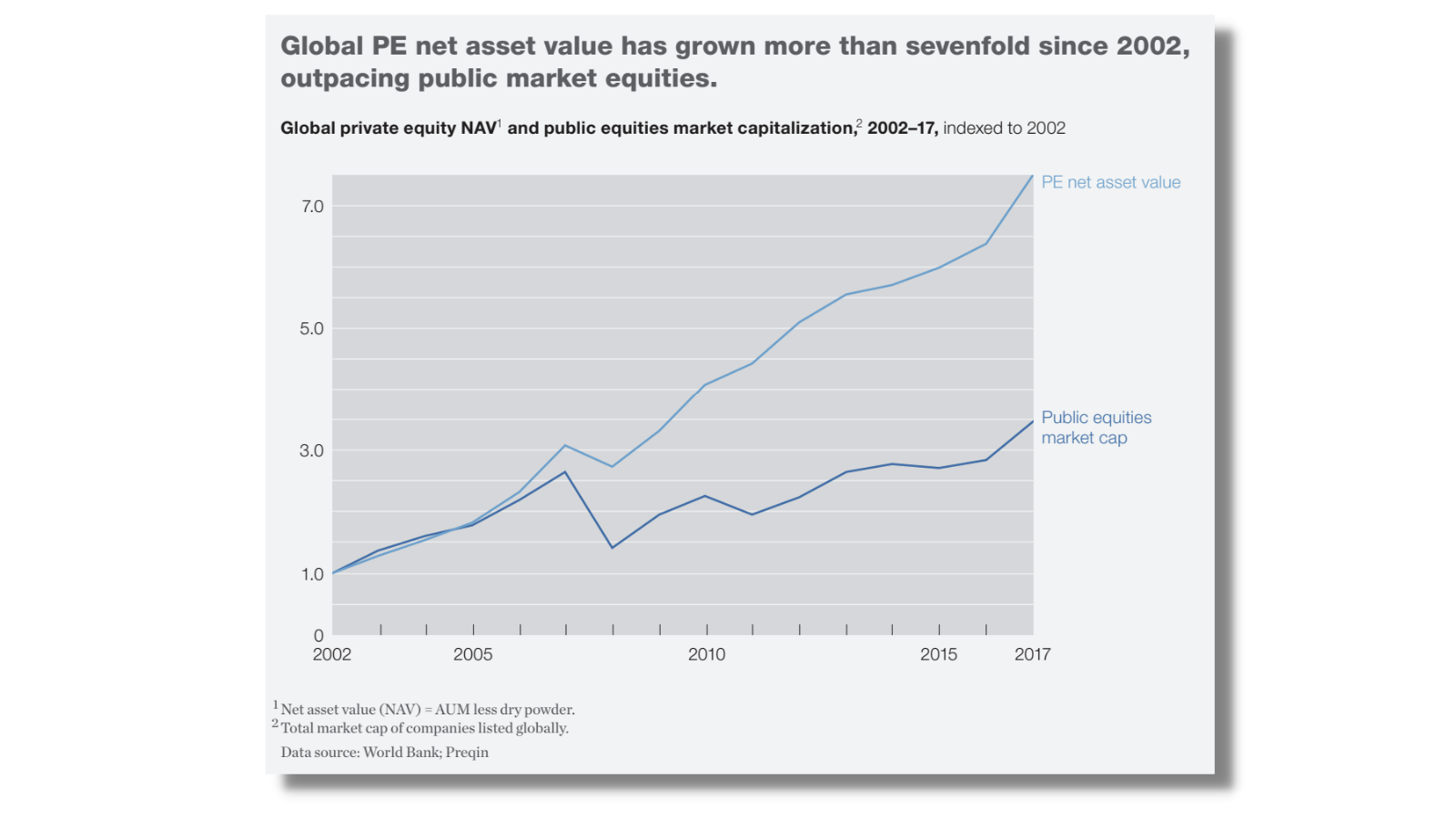

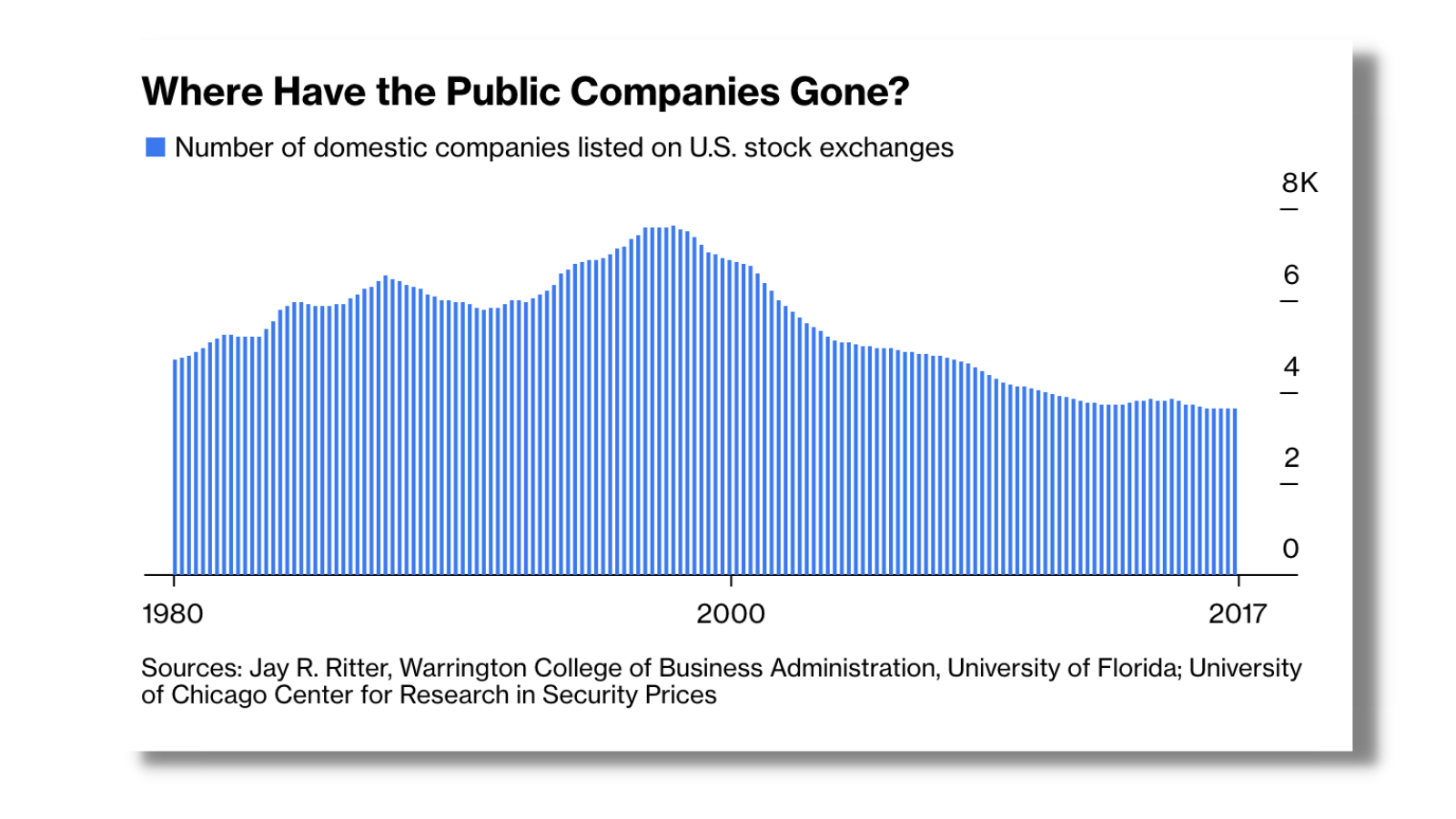

For decades, value appreciation has been shifting away from the public markets and into the private markets. The absolute number of publicly listed companies is declining. Meanwhile, global private equity net asset value grew 7.5x between 2002 and 2017, a growth rate more than twice as fast as public markets. This trend has only accelerated in the years since.

As companies stay private longer and value creation disproportionately shifts to private markets, retail portfolios are left behind. How is it that the average individual can invest in mutual funds and ETFs, but can’t invest in private equity or venture funds, let alone individual companies? For startups and small businesses, this is also problematic and limiting. Shouldn’t companies be able to tap into their communities to easily access grassroots sources of capital?

Thanks to the confluence of regulatory advances, technology innovation, and macroeconomic factors, the tides are turning. The private markets are opening, which also provides more opportunity for diverse communities to share in equity upside. Entrepreneurs building tools and platforms that democratize the private markets will shape culture and wealth creation for decades to come.

Why the 100x cap table is inevitable

There are strong tailwinds propelling the consumerization of private market investing & fundraising:

1. Everyone is an investor

The number of Americans with brokerage accounts surged +60% from 59 million in 2019 to 95 million by mid-2021, with 20 million new accounts opened in the first eight months of 2021. Today one out of five Americans actively invest in stocks or mutual funds and retail investors now account for as much trading volume as mutual funds and hedge funds combined.

This surge was bolstered by the macro environment, but the trends are unstoppable. Products like Robinhood, Betterment, Coinbase, WeBull, Toss, and AngelList make it easier than ever to invest. Online communities on Discord, CommonStock, Twitter, and Reddit have transformed into investing clubs. Consumers are also banding together to vote with their wallets, investing in opportunities that align with their beliefs and passion. Investing is officially a part of culture.

2. Community ownership

Our economic system is rooted in “shareholder capitalism” which prioritizes investor interests. The notion of “stakeholder capitalism” was born to consider a broader set of interests like employees, customers, and community members. In our opinion, stakeholder capitalism has been largely theoretical until builders in the web3 and creator economy capitalized on the concept. Today, entrepreneurs are reimagining traditional ownership models, paying creators in equity, using DAOs to rethink syndicates, or tokens to incentivize and reward stakeholders including customers, superfans, users, and contributors. (Case studies: Helium, Mirror, and Syndicate.)

A web3 startup can plausibly have a “cap table” with millions of owners. This concept is extensible to non-tokenized businesses. Beyond web3, founders are increasingly creating opportunities for early users, creators, or advisors to earn equity or invest.

We see so much value in aligning incentives via “community powered cap tables” that despite being ownership-hungry VCs, we typically cut back our own allocations to help founders better achieve this.

We're also intrigued by the opportunity to leverage web3 technology to rebuild part of the angel stack (e.g. stablecoin funding with instant settlement, smart contracts to streamline and automate waterfalls, cap table, or legal updates).

3. Regulatory changes

For most of history, only “accredited” investors (aka: the wealthy) have had the privilege of investing in private companies. In 2016, Regulation Crowdfunding “Reg CF” went into effect to allow private companies to raise from the masses. Today, companies can raise up to $5 million from unaccredited investors via crowdfunding, and must adhere to a set of disclosure requirements. This provides consumers with basic protections and information to make educated decisions.

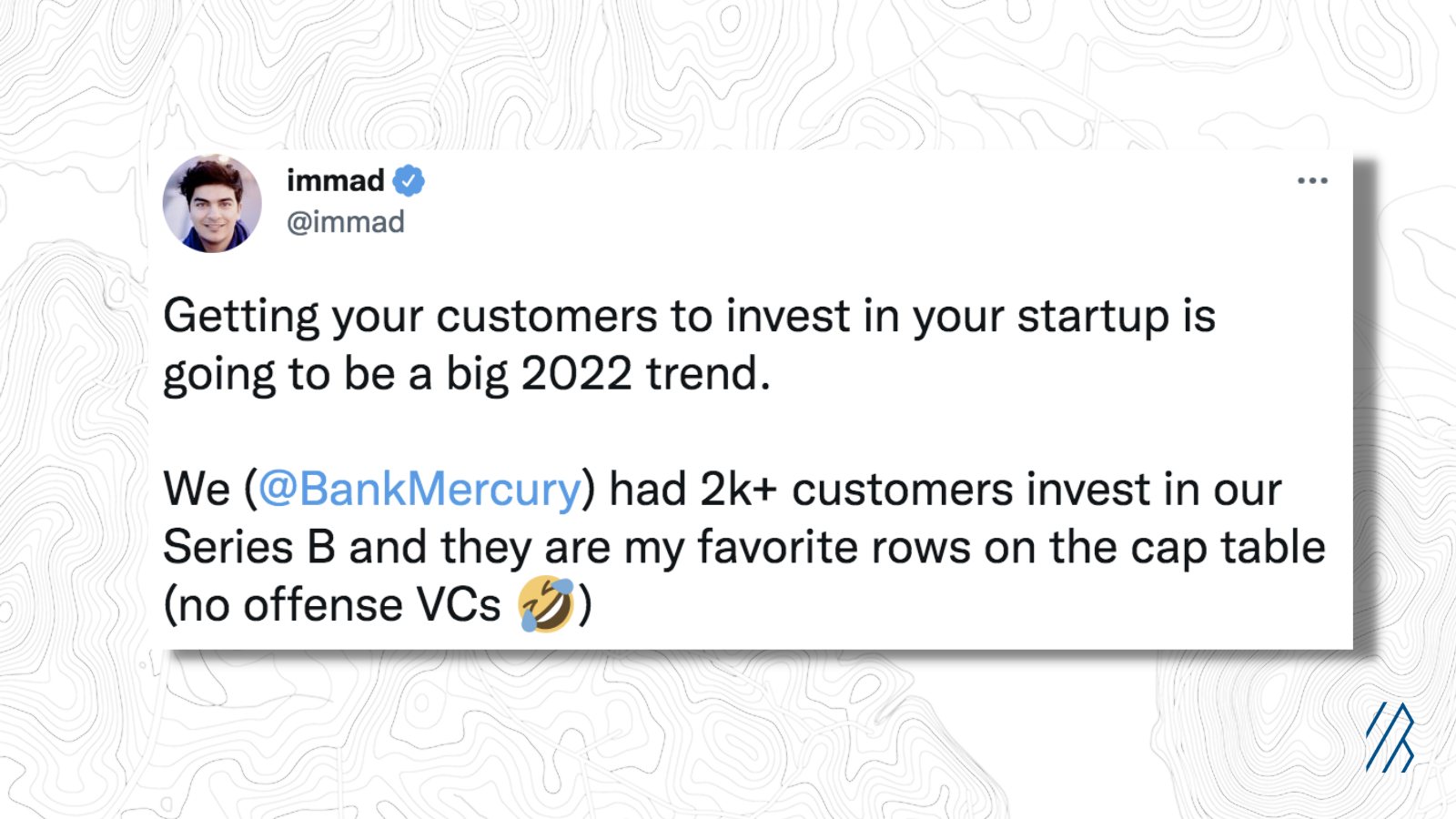

Top startups like Mercury Bank are already capitalizing on this. Mercury reserved an allocation in its otherwise oversubscribed round for customers and community members. Platforms like Wefunder and Republic radically simplify this process.

The SEC is also loosening the definition of “accredited investor.” In our opinion, this archaic concept should be abolished altogether and replaced with a short set of mandatory disclosures for private offerings. As Andy Vollmer, the former General Counsel of the SEC said, “Neither wealth nor financial sophistication can protect investors if they have insufficient information about a company.” But, at least this progress is gaining momentum in the right direction.

4. Fund and SPV infrastructure

Venture capital is being commoditized.

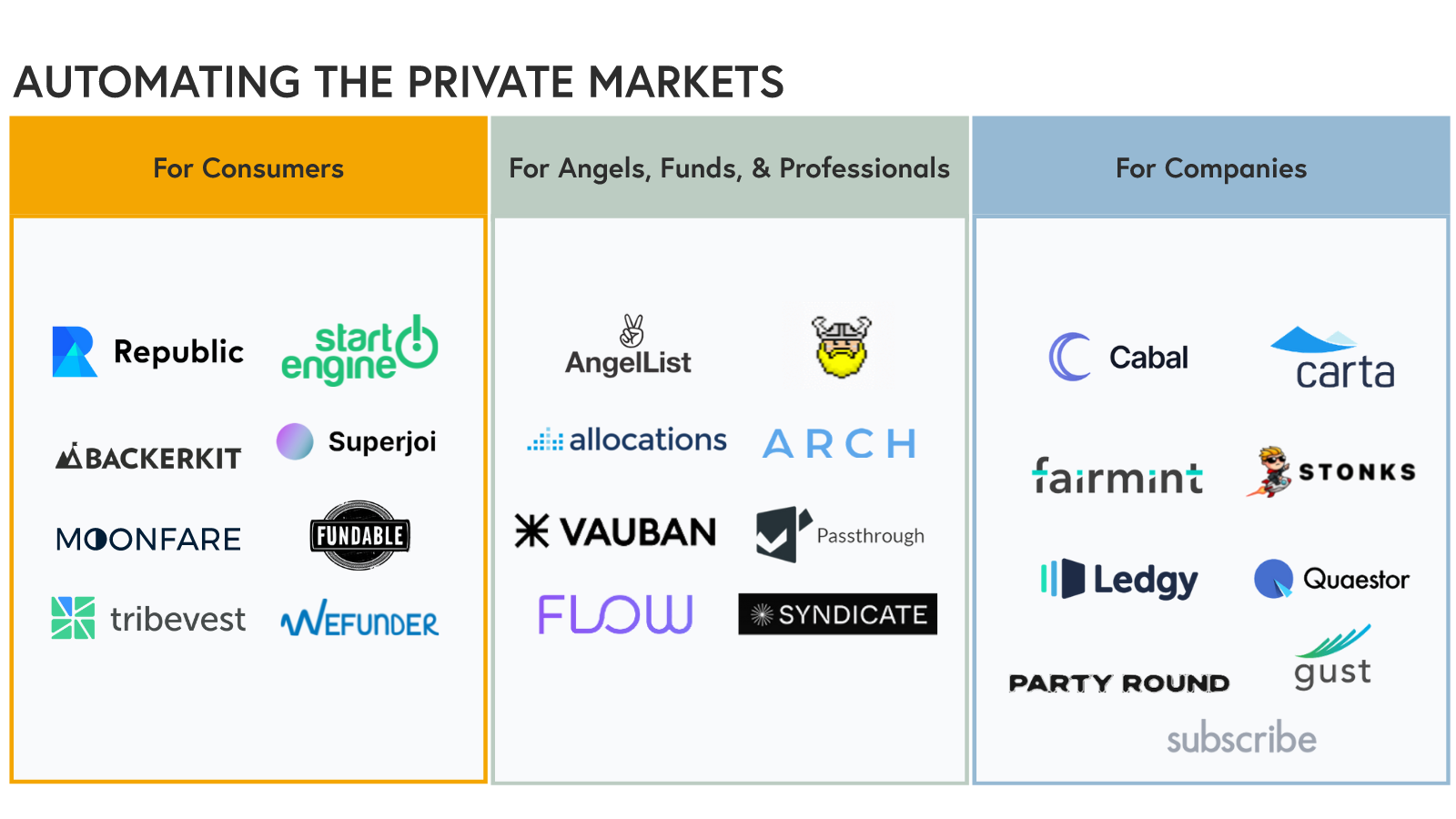

Trail blazers like Carta, AngelList, Flow, and Allocations provide modern infrastructure to easily start and manage angel funds, syndicates, etc., enabling more people to participate in the private markets. Setting up a Special Purpose Vehicle (SPV) is becoming so easy and commonplace, we suspect it will soon be a feature that some platforms offer for free! Venture capital is being consumerized and commoditized.

Hypotheses and what we are looking for to take the private markets mainstream

There is a new paradigm in private market investing and we want to meet entrepreneurs creating for this future.

We are especially interested in products and businesses that:

- Enable companies to raise money from their customers and communities

- Streamline 100x party rounds so startups can easily raise from hundreds of angels

- Incorporate community & social elements into their products and platforms

- Asset light tools, platforms or marketplaces, not next-gen funds picking investments

- Turn investors into advocates, helping companies to mobilize equity holders

- Enable PE & venture funds to easily manage large numbers of small long-tail LPs

- Leverage web3 tech stacks and concepts to automate investment processes for both web2 & web3 startups

- Bottom-up DNA, serving small startups, microfunds, and retail investors first

Open questions for the future of investing

As we consider the opportunities and challenges of this growing ecosystem, there are several outstanding questions we continue to explore.

- Angel investing is for the lucky; everyone else should be an LP: Picking individual investments is hard. This is true across asset classes. Most are better off investing in the S&P 500 than picking stocks. What is the diversified index for consumers in the private markets? As PE/VC funds scale and clamor for more capital, how can they tap into the retail market to expand their LP base far beyond fancy institutions?

- Crowdfunding: Over the past decade, we’ve seen many crowdfunding companies in the real estate and lending markets. While there have been pockets of success (e.g. REITs), the ecosystem has underperformed. What are the lessons? Will private equity crowdfunding face the same fate?

- Web3 Tech Stack: Many of the web3 decentralized ownership concepts are relevant to the consumerization and commodification of the private markets. How can the web3 tech stack accelerate the opening of the private markets for web2 companies that do not intend to tokenize?

- Adverse selection: Will the average investor have access to quality opportunities? Will companies that can attract professional investment be sufficiently motivated to include the crowd? Are consumers able to make informed decisions? These are valid questions that are actively being addressed by startups and regulators. We are optimistic that this stigma will subside as the market matures and the ecosystem evolves.

- Consumer motivation: Are financial gains the primary objective behind private market investing? How do online & offline communities play a role? The unique power of crowdfunding is as much derived from community as capital.

If any of these ideas or questions resonate, reach out to us directly by emailing us at[ talia@bvp.com](<mailto: talia@bvp.com>) and [kwalker@bvp.com](<mailto: kwalker@bvp.com>) or DMing us on Twitter at @taliagold and @kwalkytalky.