India pharma tech's next big opportunity: the sales and marketing stack

Increasing technology adoption by doctors and policy shifts are changing the business of medicine in India, and digital health companies stand to benefit.

India’s pharmaceutical market is in transition. Known primarily for producing and exporting generic drugs to other countries, India’s pharma market is on the cusp of multiple policy changes and increasing adoption of technology by healthcare professionals, particularly doctors, and domestic pharmaceutical brands and new digital health apps are poised to benefit.

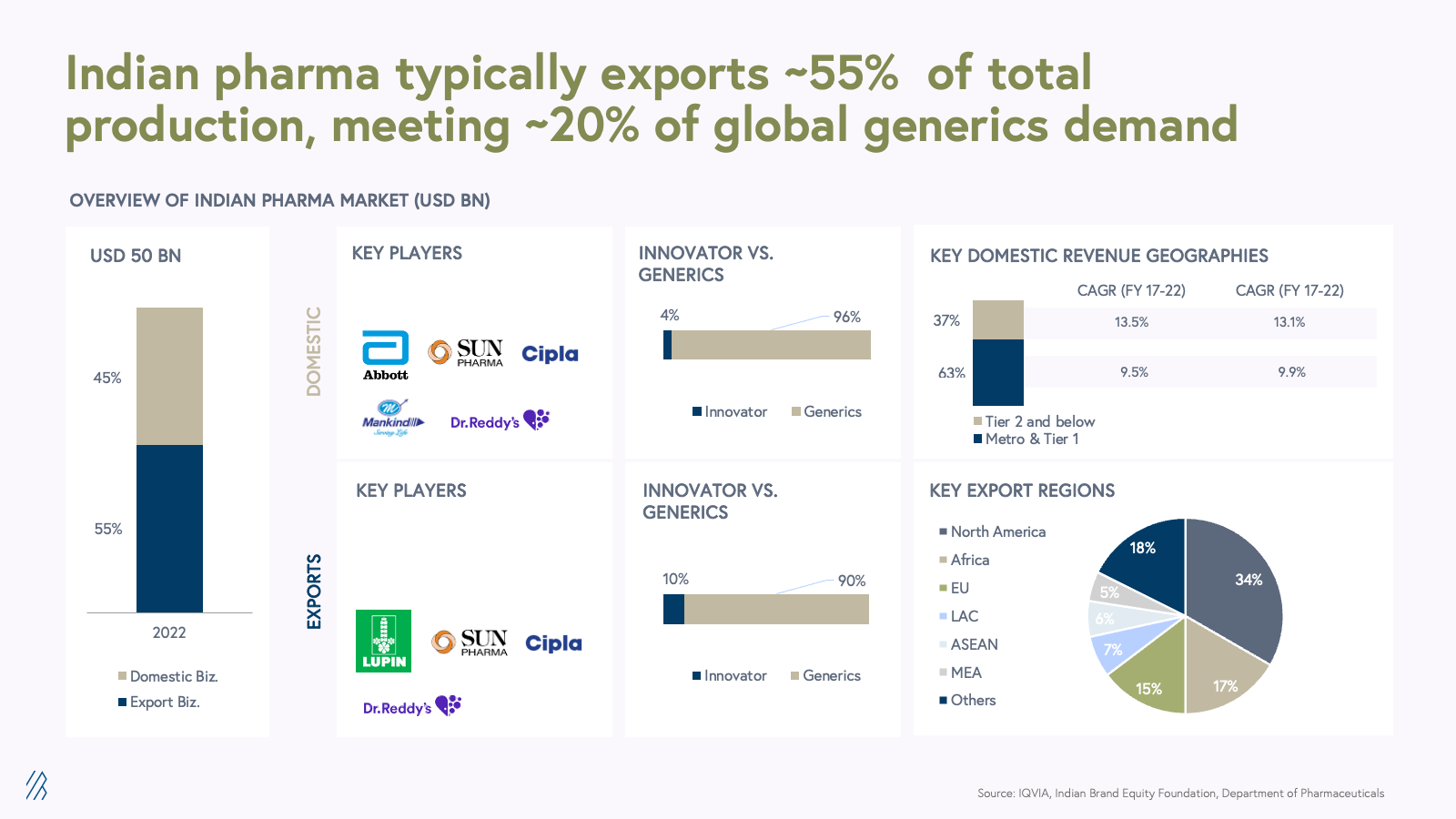

A $50 billion industry in 2023, India’s pharma market is expected to grow at roughly ~8% compounded annually over the next five years.

Innovation in pharma tech typically falls into three categories: research and development (R&D), clinical trials, and sales and marketing. Today, we see sales and marketing tech as the most significant current opportunity in India’s pharma tech market, given the scale of its addressable profit pool and industry shift to leveraging digital channels for pharmaceutical sales and marketing.

A domestic policy environment that once favored generics over new patents is now switching course––soon it’ll be easier than ever in modern Indian history for pharma companies to obtain patents for branded drugs. At the same rate, increased regulation on drug makers’ incentives to doctors are encouraging Chief Marketing Officers (CMOs) to refocus their marketing efforts toward omni-channel campaigns and digital apps.

As policy shifts stimulate growth for India’s pharmaceutical brands, digital health startups in India face opportunities to innovate across the pharma value chain, touching every aspect of drug sales and marketing, and making it easier and more efficient for doctors, patients, and distributors to engage with each other. Here’s our perspective on what’s next for pharma tech in India.

India pharma today

Historically, India has been known as the epicenter of generic drugs, catering to an impressive 20% of global generics demand. Exports constitute the majority (~55%) of India’s pharmaceutical production, with North America importing over one-third of the market’s total exports.

In India, pharma is one of the few industries whose companies are forbidden from marketing to their consumers (patients) directly. The Indian pharmaceutical industry is diligently aligning with global standards, notably those set by the U.S. FDA, through regulatory enhancements, international collaborations, and investments in quality control. Simultaneously, there is also a focus on increasing insurance penetration. While the U.S. boasts a well-established system, India is actively working to expand coverage, reflecting shared efforts to enhance healthcare inclusivity and financial protection for individuals.

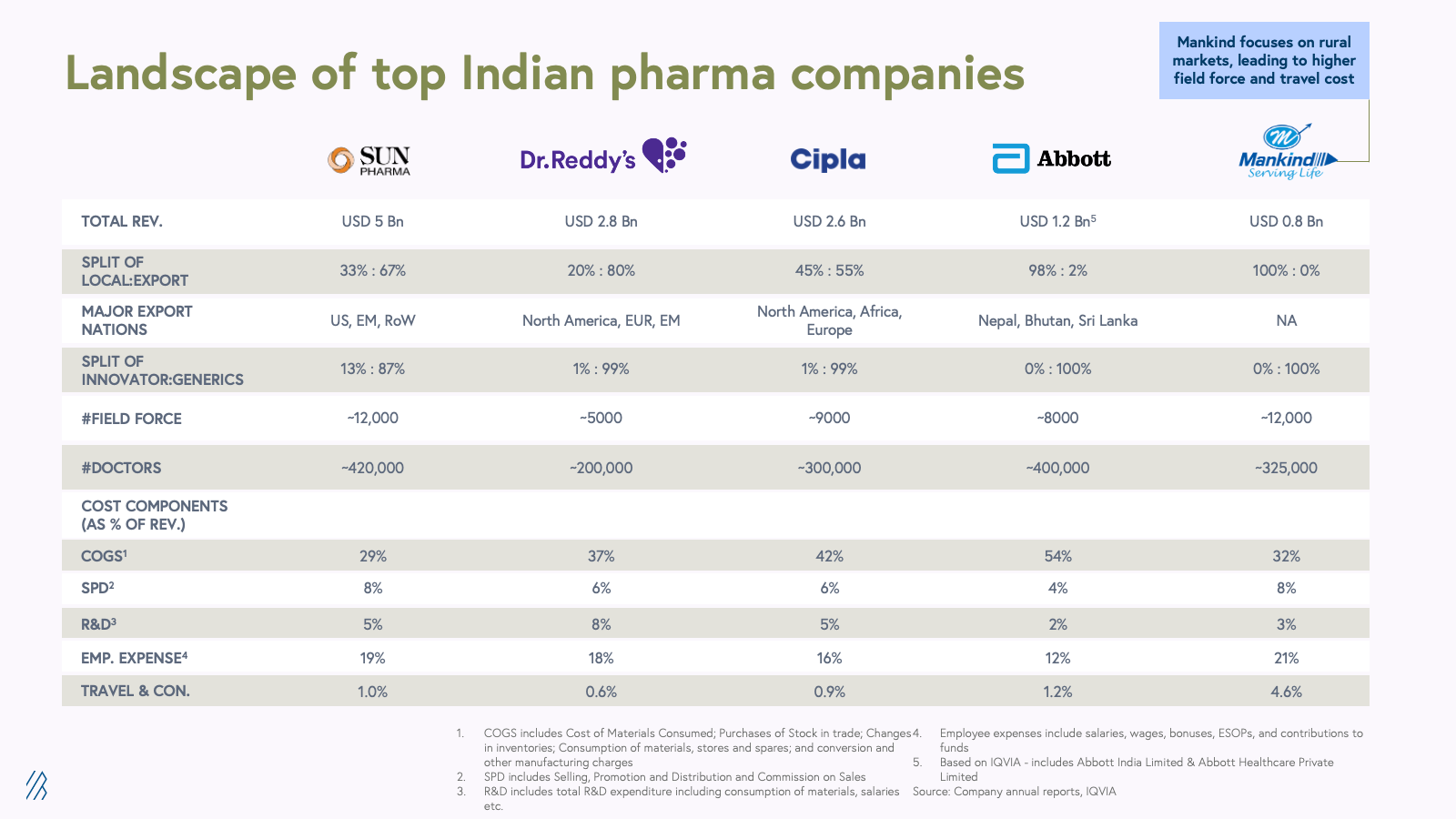

Instead, pharma companies engage with healthcare professionals, particularly doctors. Within India pharma company budgets, sales, promotion, and distribution (SPD) are a significant cost, constituting as much as 8% of revenue, depending on the company. Indian pharmaceutical giants like Sun Pharma and Mankind have strategically deployed around 12,000 medical representatives (MRs, or sales reps) each, spanning both urban and rural areas in India.

There are three main components to the pharma sales and marketing landscape: doctors, patients, and distributors. Effective pharma S&M requires engagement with all three stakeholder groups:

- Doctors: To establish meaningful connections with healthcare providers, pharmaceutical companies’ marketing tactics include conference sponsorships, medical journal subscriptions, EMR platforms, digital knowledge sharing platforms, and distributing medication samples.

- Patients: Direct marketing to patients is primarily reserved for over-the-counter (OTC) treatments. Prescription drug manufacturers in India instead look to engage patients via patient education platforms, diagnostic camps, digital apps designed to promote treatment adherence, and brand initiatives that foster trust and loyalty.

- Distributors: The pharma companies that excel in distribution tend to focus their efforts on data analytics, competitive intelligence, supply chain management, and working capital management.

Then vs. now: the provider engagement model is changing

Digital adoption has changed the way drug company representatives in India engage with healthcare providers. It used to be the case two decades ago that MRs––pharmaceutical companies’ “field force” of sales reps––would visit doctors’ offices in person for sales pitches. Armed with samples and written materials, MRs heavily relied on face-to-face interactions, engaging with doctors over the course of multiple appointments.

Doctors were initially hesitant to integrate technology into these workflows, although customer relationship management (CRM) software like Salesforce, and digital calendars, attempted to modernize doctor-MR relationships. More recently, however, the ubiquity of the internet has facilitated a gradual shift toward digital adoption in medicine in India. Digitization of healthcare became the new imperative as a result of the COVID-19 pandemic.

Today’s healthcare marketing environment requires that companies avoid over-marketing, cite scientific research, emphasize safety, and make information clear and accessible. To do this, providers and pharma companies are doing more of their work online and on software apps, and patients are engaging with healthcare content online via pharma companies’ omni-channel campaigns. Regulatory tailwinds in India are changing the landscape and accelerating technology adoption in pharma sales and marketing. Companies are looking for innovative omni-channel marketing solutions to engage with doctors. Simultaneously, there has been a notable shift in doctors' attitudes, especially in the post-COVID landscape. They are increasingly open to digital interactions with pharmaceutical companies, marking a significant transformation in the way these crucial stakeholders engage in the industry.

Why now?

In the post-COVID era, doctors are adopting technology faster than before

Digital health companies today are leveraging product-led growth strategies by selling directly to clinicians in the U.S.—the same is true for pharma tech in India. Platforms supporting healthcare professionals, in particular, are growing in popularity: as doctors shifted to end-to-end virtual treatment where possible during COVID-19, their practices required software to facilitate virtual appointments, digital assistants to maintain health records, and compliant forms of online communication, like WhatsApp-based chats and appointment booking portals. Digital health in India also extends to electronic medical records (EMRs), decision support workflows, remote patient monitoring, workforce productivity management software, and more.

Social media, too, plays an important role in India pharma sales and marketing. Doctors in India today respond better to subtler engagement from drug companies, like digital ads, as opposed to overt sales tactics from MRs.

Regulatory tailwinds

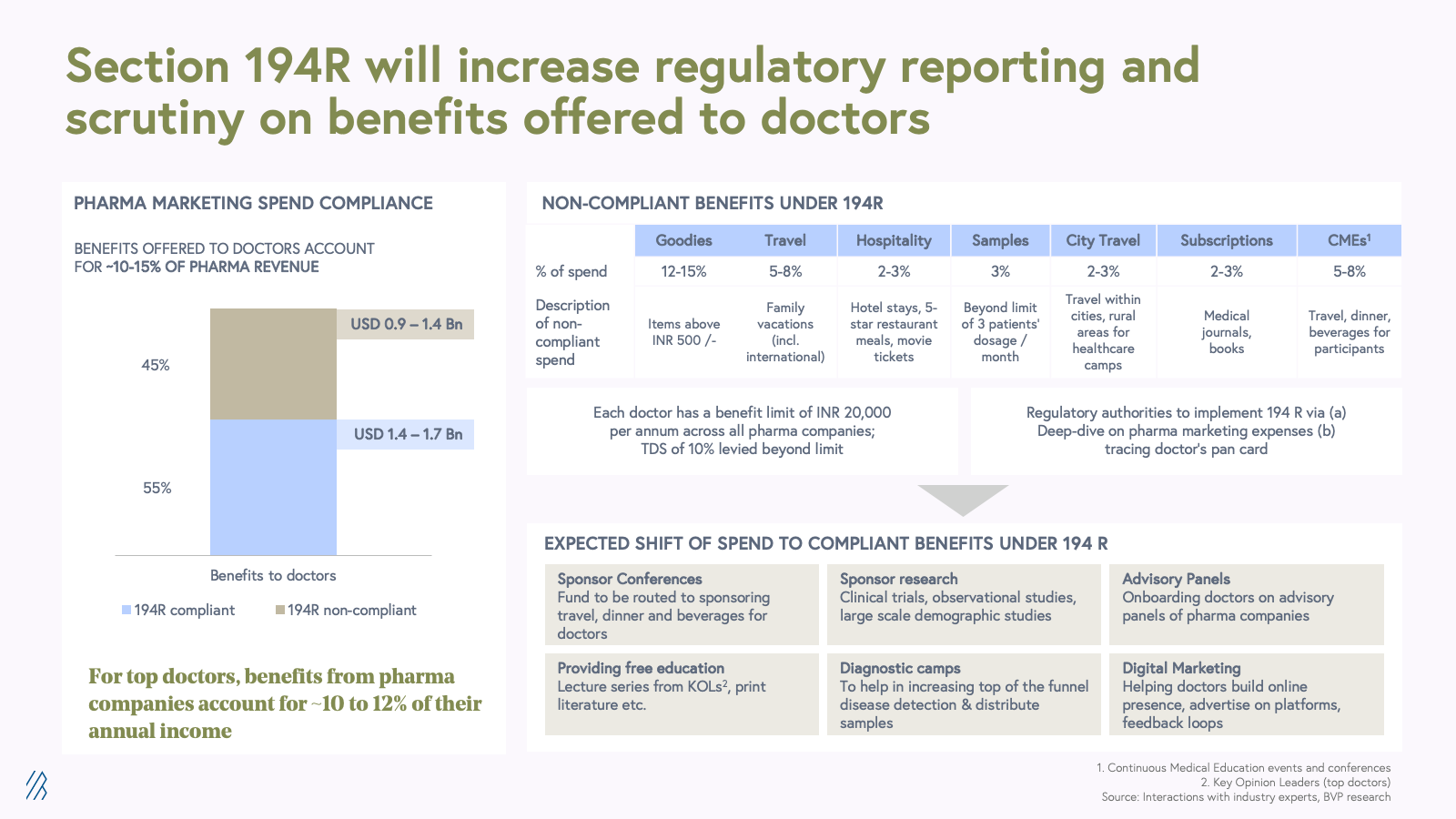

Similar to the US Sunshine Act––which curtailed and brought transparency to exchanges of value between drug companies and providers, colloquially known as kickbacks––recent policy developments in India, including Section 194R of Income Tax regulations and updated guidelines from the National Medical Commission (NMC), have intensified scrutiny on pharma companies’ incentives to doctors. Pharma CFOs and CMOs we spoke with told us that approximately 50-60% of the marketing expenditure aimed at doctors has been deemed non-compliant under these guidelines. This change is poised to create significant waves throughout the industry, given that doctors indirectly derive 10-12% of their income from pharma company incentive schemes.

As a result, a considerable portion of the pharma marketing budget is expected to transition towards more compliant methods of incentivizing doctors to prescribe their branded medications––for example, digital marketing, organizing diagnostic camps, involving doctors in advisory panels. As Indian pharma companies find new and more compliant ways to market their medications, digital adoption at each part of the pharma value chain will only grow, paving the way for innovation and competition in the pharma sales and marketing tech stack.

Key trends and opportunities

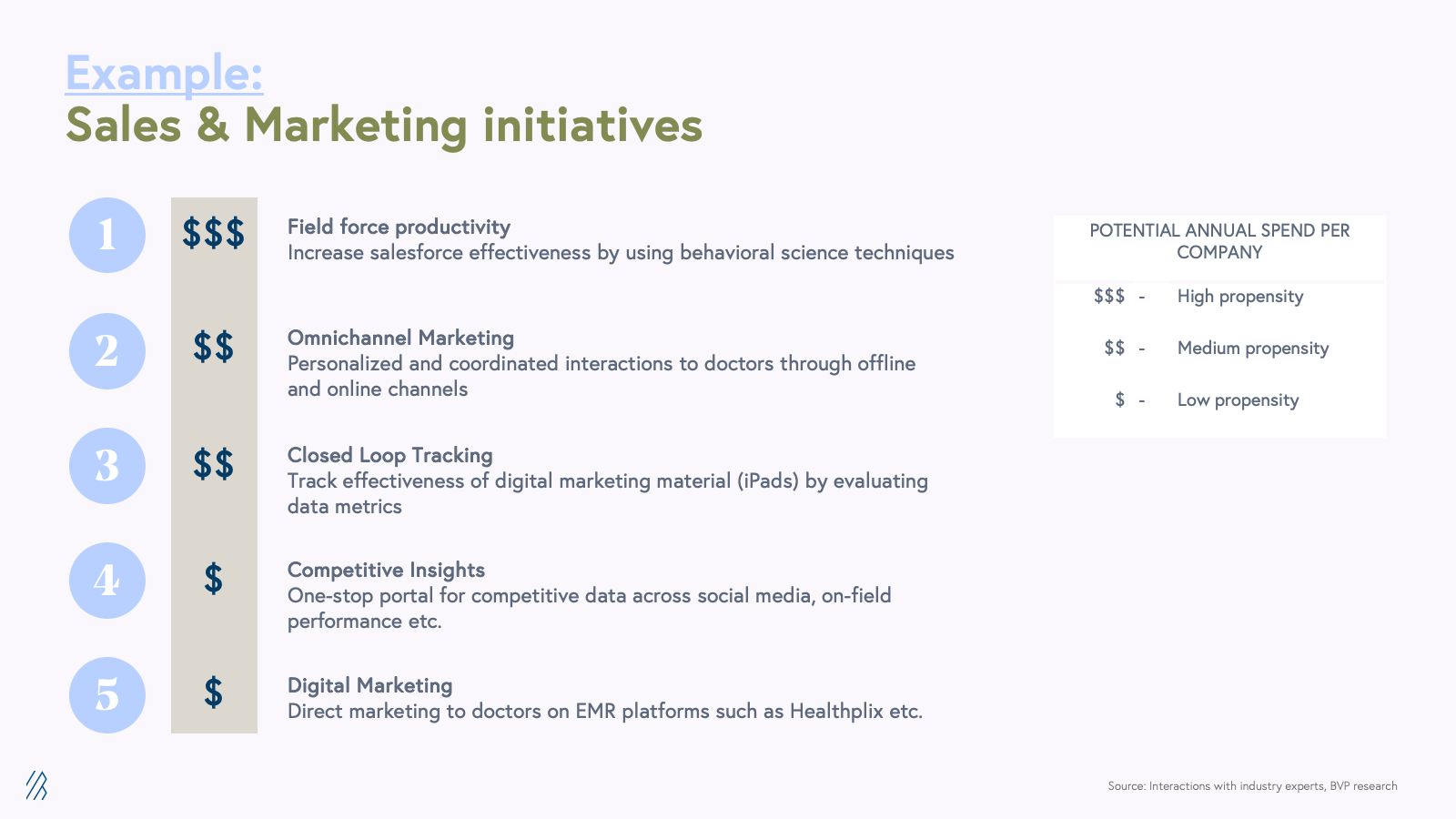

Based on conversations we’ve had with pharmaceutical company CEOs and CMOs, we’ve identified several key sales and marketing objectives: enhancing sales force efficiency, implementing personalized omni-channel marketing, evaluating the efficacy of digital investments, gaining access to competitive intelligence, and facilitating direct marketing to doctors through Electronic Medical Records (EMR) platforms.

For instance, Cipla, an Indian pharmaceutical company which primarily develops medicines to treat respiratory disease, cardiovascular disease, arthritis, diabetes, depression, and many other medical conditions, has set a goal to transition its field force onto an e-detailing platform. Instead of carrying physical pamphlets to doctors, MRs now carry iPads with content explaining how the drugs work. With e-detailing, MRs and doctors are exchanging digital content, and this new sales technique not only requires new types of digital training, but it also digitizes sales enablement, making it more cost-effective to scale over time. This is just one example of how sales techniques are being digitized. Companies like Cipla are investing in other promising startups and solutions to modernize sales and marketing practices in our increasing hybrid world within the pharmaceutical industry.

While MRs connect with physicians in new digital methods one-on-one, the industry is seeing ways to leverage content as a way to scale marketing in inventive new ways with their core audience. For example, our portfolio company MediSage is a platform focused on doctor knowledge and engagement. This online community of resources and shared industry wisdom enables pharma companies to connect with over 320,00 doctors through conferences and medical content through direct omni-channel marketing. As online portals, solutions, and digital tools persist for physicians and care providers, pharma companies will have more vertical and industry specific platforms and ecosystems to reach their target audiences.

Proactive investments in start-ups

Prominent pharmaceutical giants like Sun Pharma and Mankind have been taking proactive steps by investing in research and development, diagnostics, competitive analysis, distribution, and therapy engagement startups.

Emerging areas of interest for pharma tech in India

The Indian pharmaceutical landscape is poised for transformation. As regulatory updates change how pharma companies market their drugs to healthcare providers, we expect the India pharma market to more heavily rely on omni-channel digital marketing campaigns and apps to promote medications. To carry this out, entrepreneurs face an opportunity to innovate across the pharma value chain, building startups that enable the next generation of pharma go-to-market in India––be it a pharma-focused, end-to-end SaaS platform for sales and marketing, pharmacovigilance, and R&D, a HCP networking sight that monetizes access to data insights from pharma companies and providers, or another multi-product strategy that effectively meets emerging business needs in this area.

If you are an entrepreneur building the next groundbreaking PharmaTech software business in India, we want to hear from you. Reach out to our team at IndiaHealthTech@bvp.com.