Stablecoins: from DeFi primitive to global financial infrastructure

Stablecoins have crossed the chasm. Here's where entrepreneurs should build.

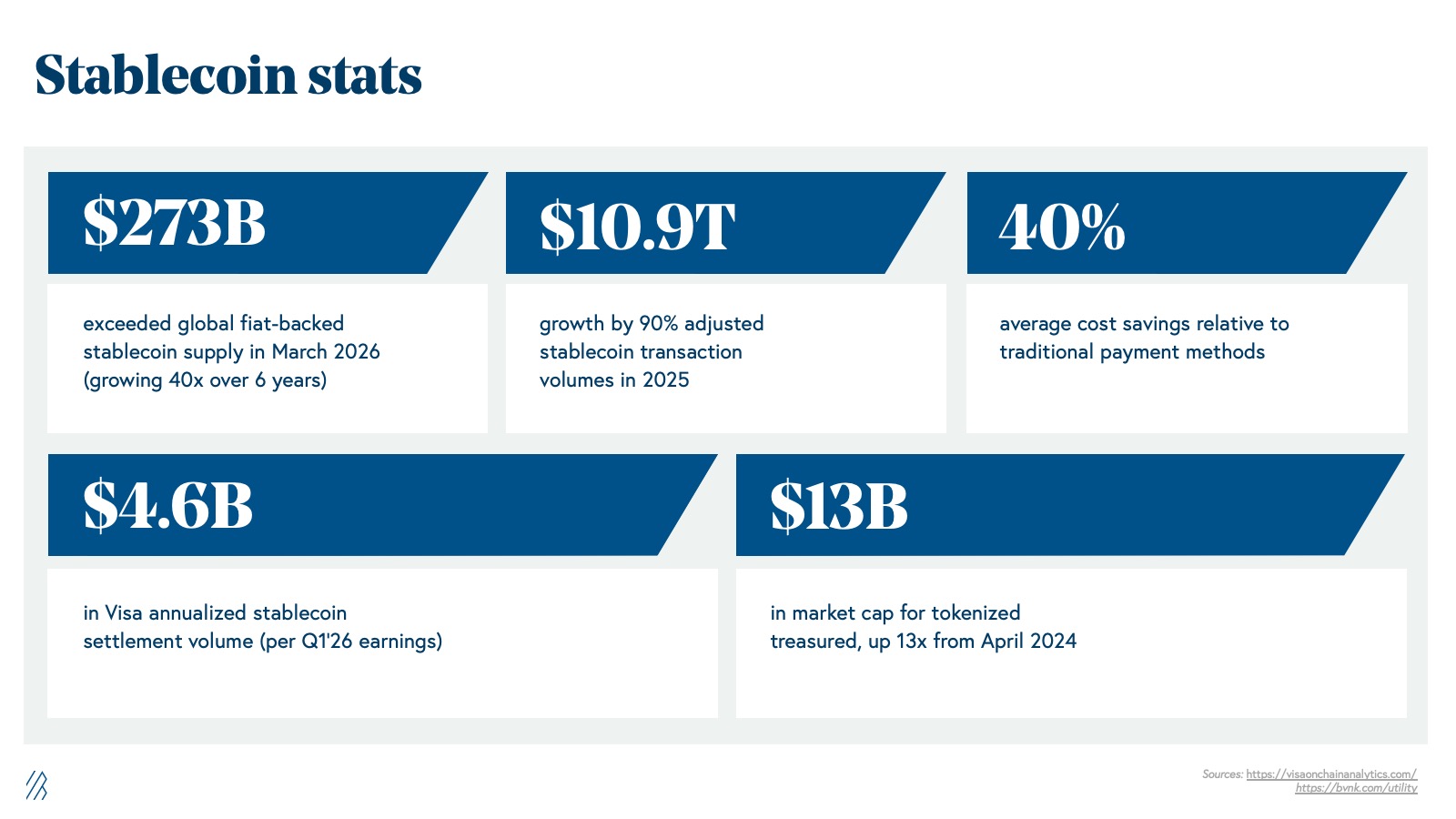

The global fiat-backed stablecoin supply exceeded $273B in March 2026, growing 40x from $6.8B in March 2020 based on Allium and Visa data. In 2025, adjusted stablecoin transaction volumes grew 91% to $10.9T, rivaling Visa’s $14.2T of annual payments volume. While the vast majority of these stablecoin flows are for crypto capital markets use cases, real-world stablecoin payments volume doubled in 2025 to $400B, 60% of which is estimated to be B2B payments, despite a falling Bitcoin price.

Stablecoins began as a liquidity layer for decentralized finance—a way to store and move value on-chain without exposure to crypto volatility. But over the past three years, the market has recognized that the core attributes of stablecoins on blockchain rails—low cost, borderless, 24/7 availability, self-custody, and programmability—unlock massive real-world applications in traditional finance far beyond crypto trading.

Our investment thesis in stablecoins—the new global money layer

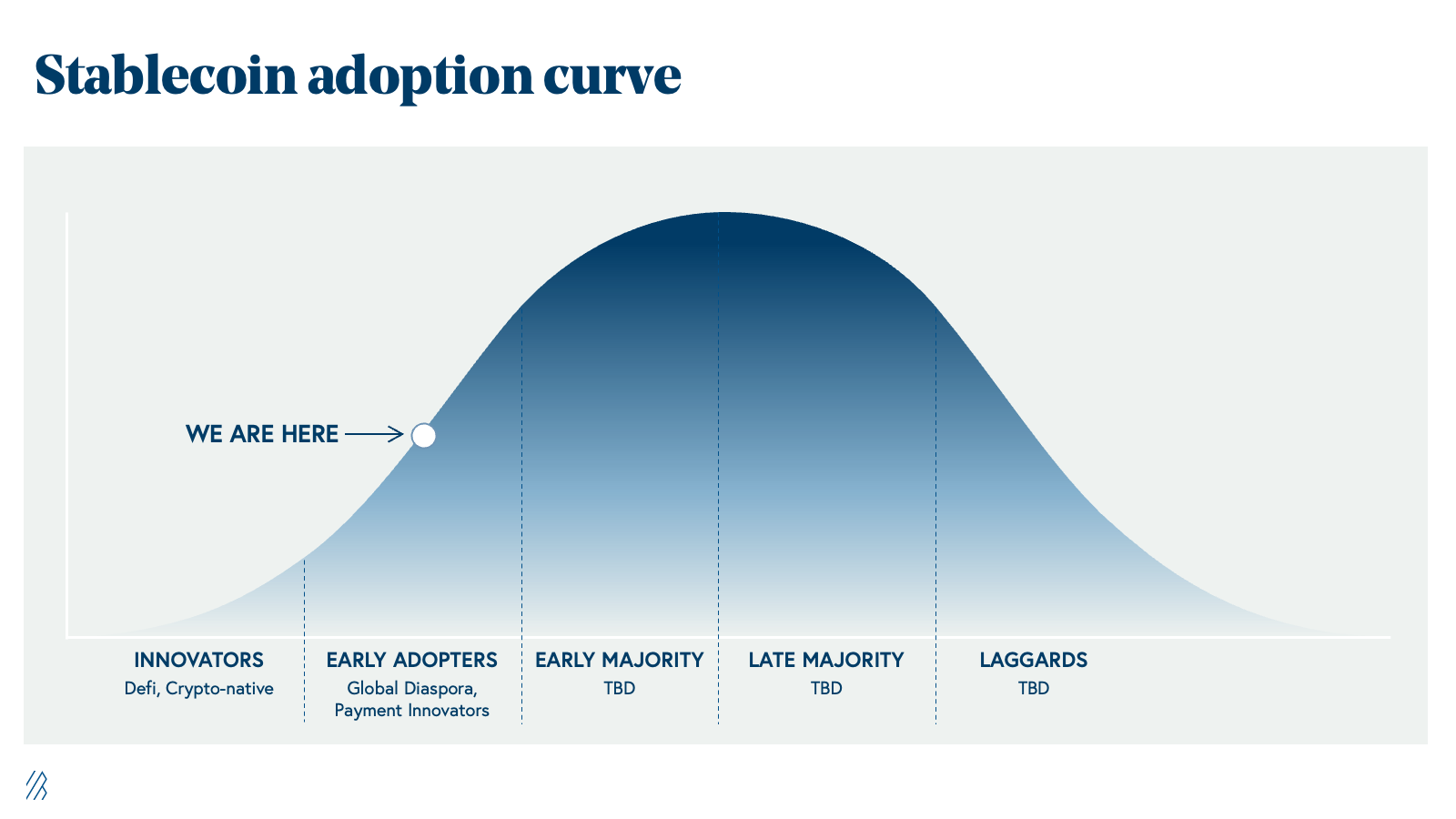

We’re still in the early innings of stablecoin adoption, but stablecoins have “crossed the chasm” from crypto-native speculation to real-world financial infrastructure. Stablecoin growth has decoupled from crypto: Bitcoin is down 50% from its peak, yet real-world stablecoin usage is growing rapidly.

The signing of the GENIUS Act in Summer 2025 solidified a federal regulatory framework for payment stablecoins, and the core tech infrastructure for on-ramp and off-ramp functionality has now been built, creating two catalysts for driving enterprise adoption. As the new global money layer, stablecoins will enable important upgrades to our financial infrastructure, making existing cross-border payments more efficient and enabling global dollar access and spending.

The true power of stablecoins

Before stablecoins, many consumers worldwide struggled to access dollars easily, and prior generations of fintechs promised instant cross-border payments but relied on pre-funding—capital-intensive arrangements where money had to be parked in destination countries before transfers could settle. Stablecoins enable “dollar” access through self-custodial wallets that transcend borders and bypass the correspondent banking network, allowing for truly instant global payments without pre-funding. At its core, a stablecoin is like a digital version of a dollar bill that lives on the internet, that you can send to anyone in the world instantly, at any time, without going through a bank.

These capabilities have opened the door to a wave of real-world applications, especially across emerging markets. They include faster and cheaper consumer remittances, dollar storage and spending in countries facing currency instability, B2B cross-border payments, freelancer payouts, and global treasury management / intercompany transfers. Outside of payments, stablecoins are also increasingly playing a role in capital markets transactions. They can enable the buying, selling, and 24/7, instant settlement of tokenized assets in contrast to traditional securities, which settle 1 business day after the transaction and only trade during market hours.

The 2026 stablecoin landscape

From 2022-2025, we saw an explosion of stablecoin startups along different layers of the infrastructure stack. In particular, companies like BVNK and Bridge, orchestrating on and off ramps, enabled significant adoption in the category at large.

On the regulatory side, the crowning achievement was the signing of the GENIUS Act, which created the first federal regulatory framework for payment stablecoins in the U.S., following in the footsteps of the European Union’s Markets in Crypto-Assets (MiCA) crypto regulation that began in mid 2024.

With mature infrastructure and more regulatory clarity in 2026, enterprises are now beginning to pursue meaningful real world applications, and we expect adoption to continue to accelerate. Visa, Mastercard, Stripe, Ramp, Meta, Cloudflare, Klarna, Western Union, Intuit, Fiserv, Zelle, and PayPal, among many other leading financial services and enterprises, have already integrated or announced plans to adopt stablecoin rails.

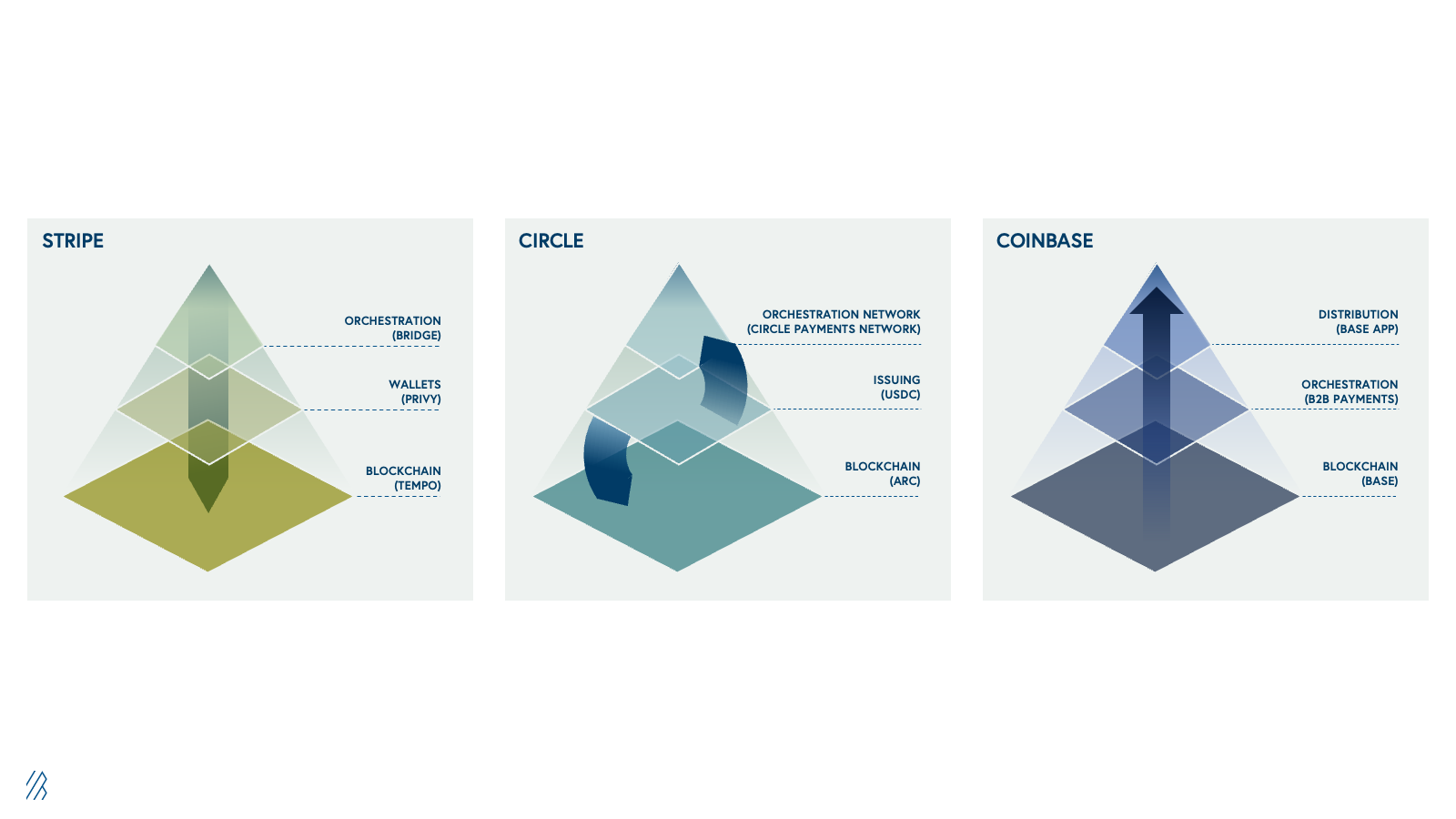

As seen across new technology cycles, stablecoin companies are beginning to consolidate functionality up and down the stack, and vertical integration is taking hold. Large companies like Stripe, Circle, and Coinbase are leveraging their distribution to become one-stop shops. This means the risk of newer startups becoming “point solutions” will grow more acute, and founders will need to be more strategic around where they are placing strategic bets.

Three examples illustrate this trend:

- Stripe’s foray into stablecoins started with its acquisition of Bridge, whose on-ramp, orchestration, and virtual USD accounts allowed businesses to hold balances in stablecoins and receive funds on crypto and fiat rails. Bridge has since launched an off-ramp product with its card product now available in less than 100 countries. Stripe then acquired Privy for its embedded wallet product, enabling businesses to hold and access stablecoins. In 2025, Stripe and crypto venture firm Paradigm jointly incubated and launched Tempo as an independent company with a new L1 blockchain optimized for stablecoin payments.

- Circle has also pursued an aggressive strategy of vertical integration. Circle began by issuing USDC and the associated minting and burning of managing the coin. In 2025, Circle then launched its Circle Payments Network (CPN), which connects partners across the world for real-time, cheap, and compliant global payments through stablecoins like USDC. Later in 2025 Circle announced Arc, a new L1 blockchain purpose-built for stablecoin finance with USDC for native gas to enable low, predictable fees, a built-in FX engine, instant finality, opt-in privacy, and full Circle platform integration.

- Coinbase has built products that span the entire stablecoin stack, from infrastructure through distribution to consumers and businesses, and is arguably the most vertically integrated player. They earn the majority of all USDC income through their role as the primary distribution partner for USDC and a revenue share deal with Circle. Coinbase has also built a full-service B2B payments infrastructure platform that offers on-ramps, virtual accounts, off-ramps, checkout, and embedded wallets. Their Base App, built on their Ethereum L2 called Base, is a self-custodial wallet in a mobile app that enables consumers to send and trade stablecoins and other cryptocurrencies.

We’re seeing a similar trend of vertical consolidation even outside of the major players. Polygon, for example, started as an Ethereum scaling chain, focused on making Ethereum faster and cheaper for developers, and then in 2025 began its expansion with the acquisitions of Coinme (licensed fiat on/off-ramps) and Sequence (wallet infrastructure and developer tools), giving Polygon the compliance, custody, and UX layers to form its Open Money Stack.

We think the most promising early stage startups building today will navigate outside the paths of Stripe, Circle, and Coinbase, and find other mission-critical spaces to generate value.

Five opportunities for startups in the stablecoin ecosystem

Despite the industry leaders pursuing an effective vertical integration strategy, we still see gaps in the market that emerging startups can fill. We categorize these opportunities across five core focus areas:

- The off-ramp problem: Wallet-to-wallet stablecoin transfers are instant and nearly free, but converting stablecoins to local fiat remains expensive and cumbersome. This interoperability gap is the most critical barrier to adoption. In a BVNK and YouGov study across over 4,000 global stablecoin users, 71% of individuals said they would use a linked debit card to spend stablecoins. Rain, a Visa Principal Member and the category leader in vertically integrated stablecoin card issuance, solves this by enabling stablecoins to be spent globally at any Visa-accepting merchant, settling directly with Visa in stablecoins. Rain’s infrastructure allows companies to compliantly issue dollar-denominated cards across the globe through a single API, enabling dollar storage and spending as a service on fully blockchain-native rails—a new product that couldn’t exist in the fiat paradigm. This is a critical and, until recently, largely missing phase in the stablecoin payments lifecycle. Once you receive and store money, you need a way to spend it. In its Q1 2026 earnings call, Visa reported that annualized stablecoin settlement volume on its network hit $4.6B.

- Enterprise-grade compliance: Enterprises will demand ironclad compliance before adopting stablecoins. These stablecoin flows ironically make compliance harder since every payment touches multiple entities (on-ramp, off-ramp, wallet, sponsor bank), each with its own Know Your Business (KYB) and Anti-Money Laundering (AML) requirements, and no institutional plumbing to coordinate across them. Infinite solves this compliance orchestration problem by unifying payments and compliance into one embedded platform with one API, one KYB flow, and one dashboard across all partners.

- Privacy: The public nature of blockchain transactions also creates challenges. Companies don’t want their competitors to see who their suppliers are and how much they’re paying them, and banks and financial institutions don’t want their trades to be frontrun or client data made public. Canton is building the first institutional-grade blockchain that is public but retains privacy-preserving transactions, while Hinkal enables enterprises to keep stablecoin transaction amounts, counterparties, and balances confidential on all major chains through a single SDK/API integration.

- Liquidity for B2B transactions: The blockchain part of stablecoin payments largely works, but the moment you need to convert between a stablecoin and a local fiat currency, the infrastructure there introduces major friction. Most real-world payment flows require touching local fiat at some point. For example, a remittance recipient in the Philippines needs pesos, not USDC; a vendor in Colombia needs COP, not USDT. A company in Miami that needs to pay a supplier in Bogotá still faces a chain of events involving liquidity providers, rate negotiation, and correspondent banks that transforms a two-second blockchain transaction into a two-day banking adventure. If large enterprises use stablecoins for cross-border payments and treasury management at scale, the ecosystem will need deeper liquidity beyond retail exchanges to maintain strong pricing with minimal slippage. OpenFX, which applies the Uniswap model to traditional FX where liquidity providers are incentivized with a share of the trading fees to provide capital to a shared pool for a given pair (e.g., USDC/AED), as well as XFX, are pursuing this opportunity. In the long-term, we may see FX markets themselves move on-chain as dollar and local currency stablecoins trade directly against each other.

- Global neobanks built on stablecoins: On the application layer, we see significant adoption of consumer remittance platforms (Sling Money, Felix Pago, NALA, Aspora) and dollar neobanks (ARQ fka DolarApp, Dakota, Karta). Companies like Revolut and Wise previously had to set up issuing, payments, and banking relationships country-by-country, which applications like ARQ can now do at once on a global level, thanks to stablecoin infrastructure. These companies are growing rapidly by delivering faster money movement, cheaper rates, and global-by-default services to consumers. Meanwhile, incumbents like Western Union are adopting stablecoin rails, demonstrated by their partnership with Rain to offer stablecoin-linked cards.

Consumer remittance is a strong case study. The model has traditionally struggled with the price sensitivity of its customer base, leading to fierce pricing pressure in competitive corridors, eventually eroding margins. New stablecoin-native equivalents can now leverage stablecoin wallets and cards to monetize like banks, earning interchange fees and a share of interest revenue on issued stablecoins, rather than just on transfer volume. The consumer value proposition also becomes far more compelling. Instead of converting dollars to local fiat upon receiving a remittance, recipients in emerging markets can store and spend in dollars directly. We see an opportunity for the best stablecoin applications to evolve from money transmitters into true dollar neobanks and scale globally much faster than their fiat equivalents by using self-custodial infrastructure to reduce local licensing requirements.

The next frontier: tokenization, agents, and beyond

The tokenization opportunity

Once businesses and individuals hold stablecoins, they’ll naturally seek returns. This opens the door to tokenized treasuries from Circle and BlackRock, active yield generation through protocols like Morpho and Aave, and tokenized equities offered by Ondo, xStocks, and Robinhood. The New York Stock Exchange recently announced a partnership with Securitize to build a blockchain-powered trading platform for tokenized stocks and ETFs, enabling 24/7 trading and instant settlement with stablecoins. In mid-March, the SEC approved Nasdaq’s proposal to allow certain stocks to be traded and settled in tokenized form.

Since April 2024, the market cap of tokenized treasuries has grown 13x, from $1B to nearly $13B today. The tokenized stocks market, which effectively didn’t exist two years ago, has more than doubled over the past year to $945M. As the big players continue to enter the space once regulatory clarity is established, we expect both markets to accelerate.

Within the US, security tokenization represents the potential of a core upgrade to our financial infrastructure. For emerging markets, the long-term opportunity could be a dollar neobank that offers a stablecoin account, cards, and seamless access to tokenized U.S. treasuries and stocks, enabling global access to the US financial system.

Agentic payments

Cloudflare recently announced NET Dollar, a U.S. dollar-backed stablecoin designed for the agentic web. As AI agents continue to improve and increasingly take autonomous economic actions online, it’s possible that traditional payment rails may fall short since card networks and cross-border fees make microtransactions uneconomical, and batch settlement is mismatched for agents operating 24/7/365. Leveraging stablecoins, Cloudflare envisions pay-per-use pricing and microtransactions that enable creators, developers, and AI companies to monetize in ways that weren't possible before.

We're excited for more entrepreneurs to imagine new stablecoin use cases that fall outside the scope of traditional payments.

How we evaluate stablecoin startups right now

At Bessemer, we look for five key criteria when meeting founders in this space:

- Real-world value creation: the best stablecoin startups either make a traditional financial offering meaningfully more efficient or deliver a net-new product to a non-crypto-native customer that couldn't have existed before.

- Vertical integration: controlling key parts of the underlying stack to maximize unit economics and reduce counterparty risk.

- Ease of use: fully abstracting away the complexity of blockchain, custody, and key management—so easy your grandmother could use it.

- Global by default with clear multi-geo product-market fit (PMF): scaling across many countries from day one, which expands TAM and diversifies regulatory risk.

- Rapid yet compliant growth: growing fast but with a deep respect for compliance and a willingness to invest in long-term sustainability.

Fundamentally, we believe stablecoins are poised to become the next-generation, global-by-default financial infrastructure layer as new fintechs will use stables and self-custodial wallets to grow faster and go global earlier than ever before. We're actively investing in founders who combine deep traditional finance/fintech and crypto expertise to both rewire existing financial services and pioneer new products that couldn’t exist on fiat rails. If you’re building in this ecosystem, we want to talk to you. Reach out to Charles Birnbaum, Eric Kaplan, and Brandon Nydick.