Inside the biggest bet in corporate history

The hyperscalers keep raising their stakes on AI capex and will soon have $8T+ in the pot. Is this brilliant or reckless?

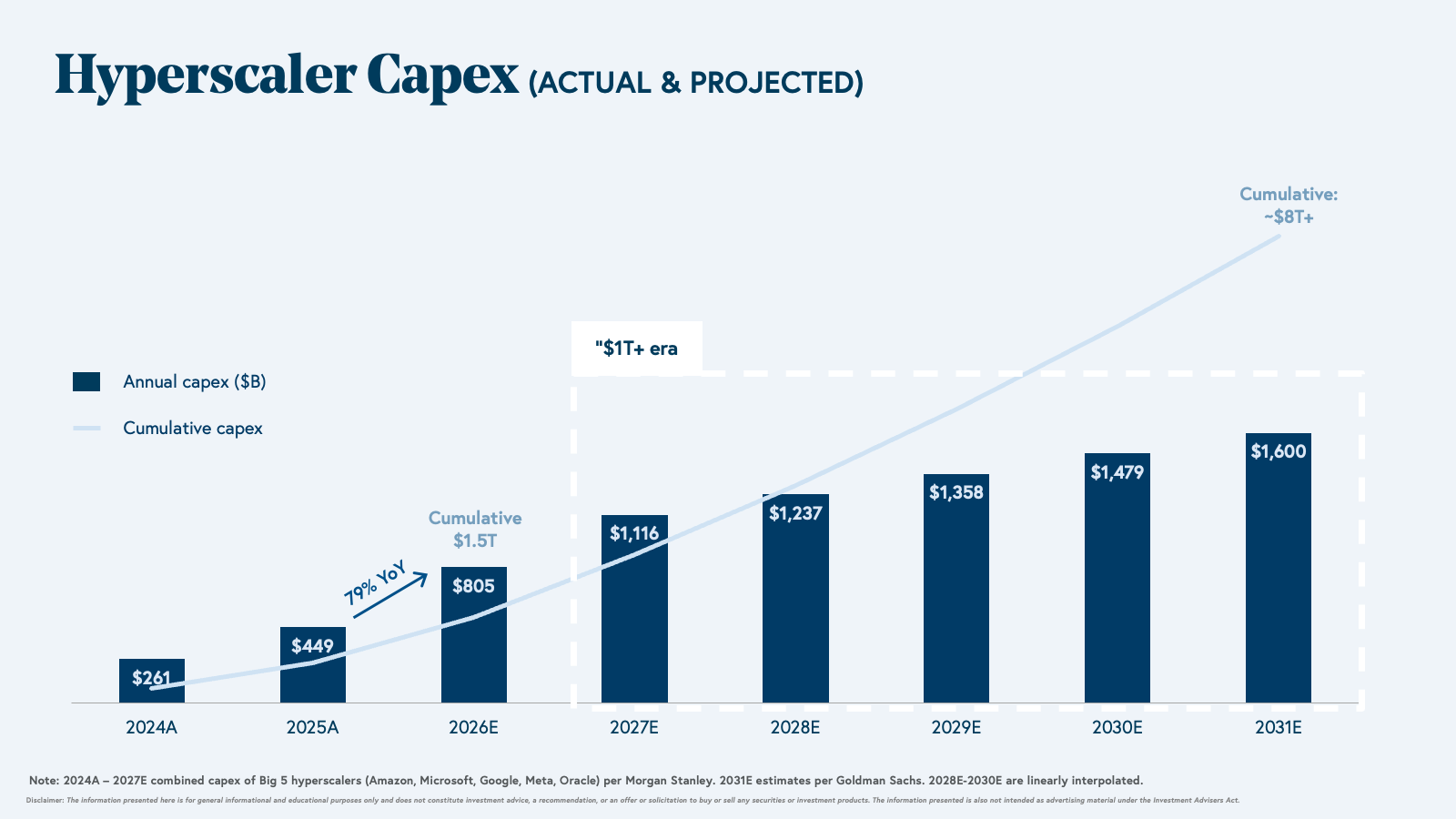

The hyperscalers are making the largest bet in corporate history. By next year, capex from the big five (AMZN, MSFT, GOOGL, META, ORCL) are expected to cross $1 trillion per year. Cumulatively from 2025 to 2031, roughly $8 trillion1 will go into the ground, running parallel with the entire yearly U.S. Department of War budget over the same period. Hiding inside that bet is AI’s biggest moment.

The private industry has never attempted anything close to this magnitude, which begs the question of what you need to believe for it to pay off. Plenty has been written about the supply side: GPUs, data centers, and power as the hyperscalers, neoclouds, and AI labs focus on supporting skyrocketing inference and training requirements. However, the more interesting question is what this build-out implies for the demand side, and the AI value creation event hiding inside the math.

If you build it, will they come? For every $1T of ramped Capex, hyperscalers need $500B in incremental yearly revenue

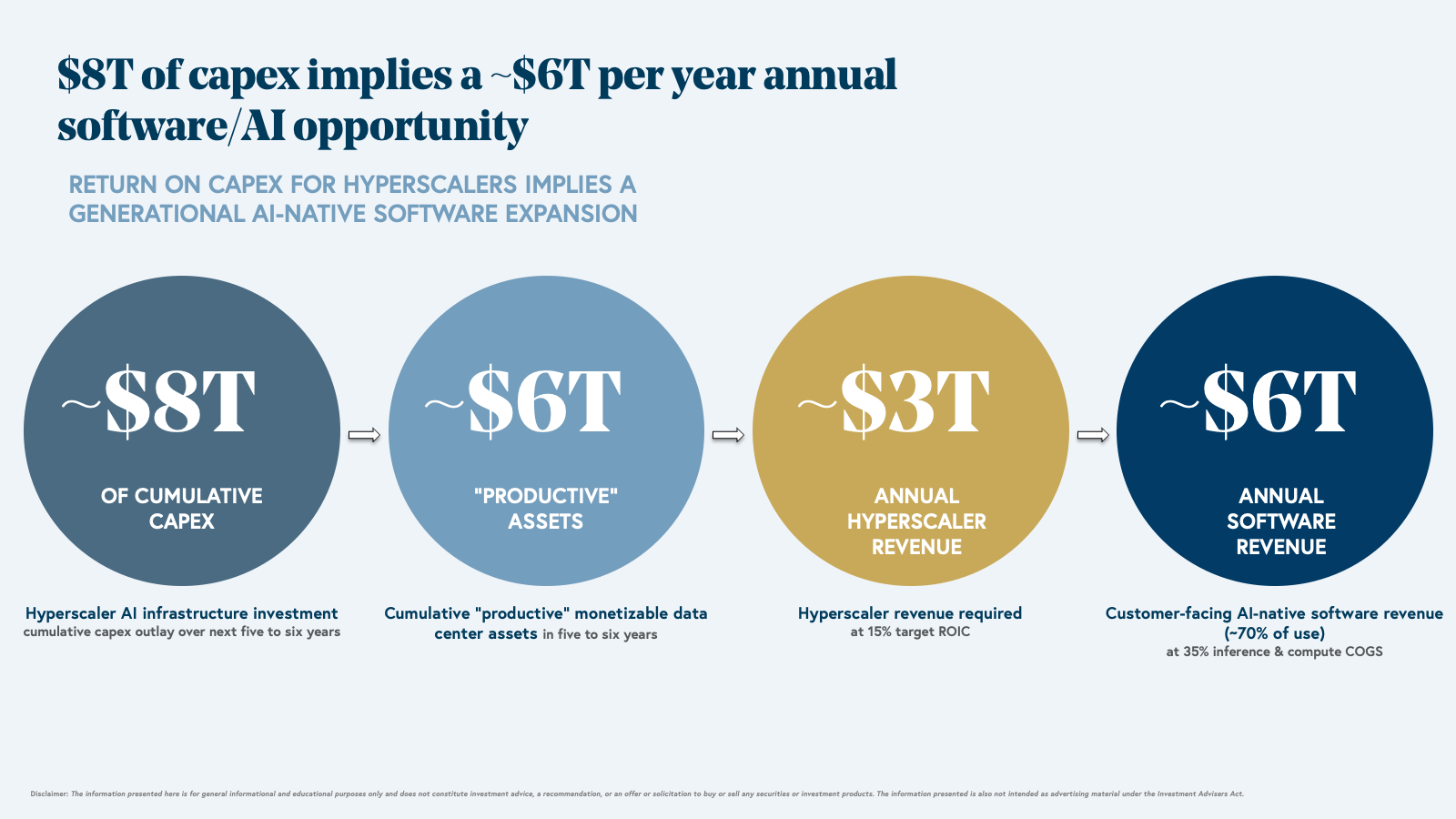

For the hyperscalers to hit an unlevered 15% ROIC, each $1T of ramped capex would yield $500B in annual revenue (at ~30% margins). Apply that to the full build-out: under a three-year ramp to full productivity, $8T of cumulative capex translates to $6T of productive assets in the next five to six years. This $6T base of ramped assets would imply $3T of incremental annual hyperscaler revenue, ~7x growth from ~$450B expected for 2026E.

Working one layer up the stack: if ~70% of compute serves external AI applications, and those applications spend ~35% of revenue on inference & compute COGS, then ~$6T of customer-facing global software revenue would be needed to justify these expenses2.

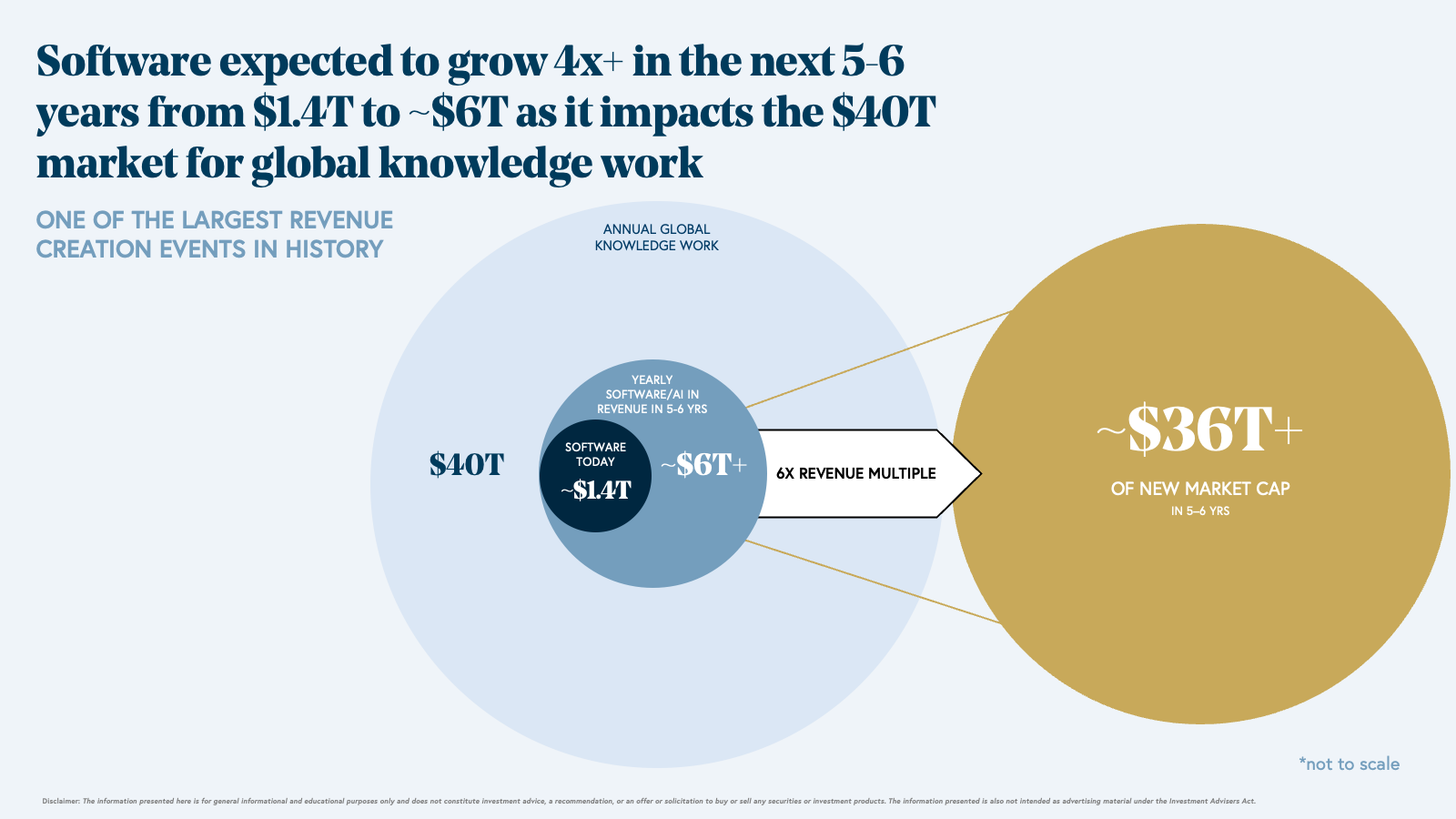

Compare that to ~$1.4T of global software revenue today. That’s 4x+ growth in the next five to six years or an average CAGR of ~30%. This growth may come in many forms and could be one of the largest revenue and value creation events in history.

Largest greenfield money-making software opportunity in history

This is the largest greenfield money-making opportunity in history. Not just in software. Not just in technology. In all of business. Most of it is still unclaimed. The winners won't look like the previous generation of cloud leaders. They'll be AI-native from inception, with tokens as the fuel, and outcomes as the unit of value. AI applications will displace incumbent services revenue and expand the categories.

The main prize is the $40T+ paid annually to knowledge workers globally: legal, accounting, consulting, healthcare administration, customer support, sales, recruiting, claims processing. All of these categories will expand and evolve in the new paradigm. The next generation of founders is rebuilding the service itself as software.

In five to six years, if valued at a 6x revenue multiple, the $6T revenue opportunity implied by the hyperscalers would represent ~$36T+ of new market cap (and as the capex cycle continues, it will only continue to climb). If it doesn't materialize, the capex doesn't pencil. For reference, the total enterprise value of all global public and private companies (equity + debt) is ~$260T+. $36T of value creation would equal ~14% of the entire global corporate ecosystem.

Hyperscalers are laying the groundwork for the new generation of companies. Platforms that make inference and training cheap, fast, and reliable will be part of the new infrastructure fabric. The picks-and-shovel economy is already in motion at every level of the stack: orchestration, evals, observability, fine-tuning, memory, inference, agent runtime, data management, networking, and more. Numerous generational infrastructure companies (Snowflake, Databricks, Datadog, MongoDB, HashiCorp, Confluent) were built on top of cloud. The same wave is coming for the AI stack (and the energy stack), and it's still early innings.

The winners

We think the demand will pull through, and that the winners of the AI era will be more distributed than people expect.

The key way this AI wave will be different from the cloud wave is how the economic value will split among the layers of the stack. Hyperscalers captured an outsized share of wave one cloud-era market capitalization. That won’t be the case this time.

Nvidia, Broadcom, AMD, and other hardware vendors have captured the early value. Hyperscalers are now benefiting from the demand surge, and will continue to in absolute terms. Cloud compute revenue growing from $450B to $3T+ means players such as AWS, Azure, and Google Cloud would collectively generate trillions of dollars of new value. But this is just the first inning. Hyperscalers don't have the same software IP position in this wave (especially at the foundation model layer), and they don't have the same market power against the layers above them.

As the value and relative leverage rotates up the stack, foundation model companies such as Anthropic, OpenAI, Google Gemini, and SpaceXAI will scale rapidly. We believe additional AI infrastructure software, platforms, and AI-native applications selling outcomes will fast follow.

Multiple trillion-dollar software companies of the 2030s are being built right now.

The $36T+ unlock is happening and it's going to be a wild ride.

Disclaimers

The information presented here is for general informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer or solicitation to buy or sell any securities or investment products. The information presented is also not intended as advertising material under the Investment Advisers Act.

Certain companies discussed may be current or former portfolio companies. BVP may still have a financial interest in these companies. Any discussion of specific companies, securities, or investment strategies should not be considered a recommendation to take any particular action. Past performance is not indicative of future results. All investments involve risk, including possible loss of principal. Market conditions and investment returns can fluctuate significantly. Please visit https://www.bvp.com/legal for more information.

1 Morgan Stanley and Goldman Sachs Projections

2 A portion of hyperscaler capex serves vertically integrated workloads (search, ads, ranking, internal model training), where economic returns show up in downstream hyperscaler revenue lines. For simplicity, the analysis assumes the return shows up in customer-facing revenue.