The antidote to cryptophobia

Our crypto optimism and why we believe in the promises of blockchain technology.

Comparisons between the advent of the Internet and cryptocurrency are so overused as to be trite and meaningless these days—except for one important thing. We experience paradigm shifts slowly at first and then all at once.

As a 14 year-old, I (Ethan) remember the day. First, my state of mind: mental rapture would be an overstatement, but curiosity and intrigue wouldn’t be far off the mark. I was an intern at the venerable Boston law firm of Hale and Dorr and the firm’s “Computer Services” leader had shown me the World-Wide-Web courtesy of the National Center for Supercomputing Applications, an until-then obscure state-federal partnership housed at the University of Illinois. Navigating around the Web circa 1992, there was a grand total of zero well-known organizations embracing this potentially world-changing new communication medium, but I was enthralled and must have visited the random hodgepodge of physics labs (SLAC and KEK) and the genesis website, CERN’s introduction of the “World-Wide-Web project” too many times to count. The utility of this new tech wasn’t entirely clear, but it was novel and auspicious enough that it met the low bar for me of “cool,” a bar I might add that for a 14 year-old law firm computer division intern might not have been worth a lot in most contexts but still was something of a harbinger of where my career would go next. “Check this thing out and figure out if we should have one of these,” the leader—my internship sponsor and boss—suggested. Enough said, I was on my way.

The early commercial promise of the Internet had small victories—at least in my (Ethan’s) circles as a cute advertising medium for putting law firm brochures, practice pages, and attorney bios out into the world—before giving way to disappointment about the lack of truly commercial applications. Cool wasn’t enough to get people to pay attention. Useful was.

Crypto is having that same existential crisis of confidence now.

It’s with an eye on both the past and future that we are excited to engage with our respected colleague Adam Fisher on his cryptophobia. We couldn’t brush off Adam’s genuine concerns about the potential impact of blockchain-based applications and tokens—especially because he’s not predicting failure but more worrying about the potential consequences of success. We had no choice but to pay attention to these kinds of ominous premonitions from such a thoughtful source.

We’re far more optimistic about the tangible use cases blockchain and crypto uniquely enable, in the same vein with the idea that technological changes will only continue to better society.

In our rebuttal to Adam’s cryptophobia, we focus on the compounding growth of developer and builder activity over the past few market cycles, our thesis on why gaming is the perfect initial roadmap for the space, and the need for policies and regulation to keep the space away from complete implosion, all the while ensuring the benefits are more universally shared. A progressive future iteration of the Internet will focus on decentralization of power and dispersing that power across the hands of the builders and creators of the web.

The case for optimism (aka our rebuttal to Adam)

It’s true, many cryptocurrency advocates resemble zealots and justify their actions presupposing you agree with their premises—often grandiose and anarchic in nature. This sort of self-referential business plan—full of assumptions that make the business viable—is rife in the world of crypto startup pitches. As we settle into the next crypto winter, we believe the fundamental core innovation is having and will have tremendous impact. Crypto skeptics may be throwing the baby out with the bathwater in letting their inner anxieties about the socio-utopian aspects of crypto trump some of the practical technological advancements.

This is history repeating itself with the Internet, e-commerce, social media, and other more bleeding edge innovations like VR and AR as well. Writing for Newsweek back in 1995, well-known prognosticator Clifford Stoll expressed his deep concerns:

“I'm uneasy about this most trendy and oversold community. Visionaries see a future of telecommuting workers, interactive libraries, and multimedia classrooms. … And the freedom of digital networks will make government more democratic. Baloney. Do our computer pundits lack all common sense?... What's missing from this electronic wonderland? Human contact. Discount the fawning techno-burble about virtual communities. Computers and networks isolate us from one another. A network chat line is a limp substitute for meeting friends over coffee.”

Stoll wasn’t wrong about the potential unintended negative consequences of the Internet, but he missed the other side of the coin and as such, paints all of such a multifaceted innovation with one brush: pessimism of concern as opposed to excitement or curiosity for the future positive benefits. We are loath to a make a similar mistake here—and feel it would be wrong to ignore the many positives that have already been unleashed into the world with the advent of programmable blockchains first envisioned by the Bitcoin White Paper in 2008—and of course even dare to dream a bit about the future unrealized promise of such a low-level and extensible technological concept.

When our partner David Cowan incubated a roadmap in the early to mid-1990’s simply called “The Internet,” he theorized that this new decentralized protocol would fundamentally change the way we communicate and conduct business. As Gilad Edelman describes in “Paradise at the Crypto Arcade,” the internet was designed to be decentralized with a “very practical Cold War-era purpose: a network of computers spread around the country couldn’t be wiped out in a single nuclear blast.” We think a similar adage applies here.

In fact, it’s no stretch to posit that the collective “we” has come to the realization that the internet may not have ultimately developed solely in its intended virtuous way. In fact, the opposite has often turned out to be true for consumers; network effects have driven nearly monopolistic ownership of attention across major platforms. Web3 skeptics’ disdain for token-driven incentives should examine why, for example, paying miners to validate transactions or compensating creators for content they produce is morally or economically worse than padding the bottom line of the cloud computing oligopoly’s balance sheets or using consumer data to manipulate behavior towards addiction, sell products, or both. Both the open-source ethos of blockchain and its practical implications for developers have led to increased customization of the user experience, as well as the potential for more economic equilibrium between platform and consumer.

I (Lindsey) grew up in a different era of the internet. “Creators” weren’t called that yet—they were just beloved personalities who represented the quirkiest parts of the internet (admitting YouTube was your primary form of entertainment was nowhere near as cool as it is now), or specific communities that were nearly impossible to find represented in mainstream media. My friends and I would host watch parties when Wong Fu short films were released, over a decade before Asian American talent could be readily found in traditional film and television. However, the stats on making a living on YouTube for the long tail of creators are dismal (roughly $3-5 per 1k views), and platforms have trained audiences to think of new-age media content as “free”—untrue as user data is harvested for advertisers—which forces creators to set up donation pages on Patreon and other platforms, supported exclusively by the altruism of their superfans. The same can be said for up and coming musicians who, without distribution, cannot afford to live off the pennies of royalty payments from streaming services.

Crypto offers an alternative: creators, particularly those large enough to be distribution channels themselves, can engage directly with fans (versus going through their labels and negotiating both masters and publishing rights, or receiving only an aggregate view of listeners from streaming platforms).

For example, Grimes sold $6 million worth of NFTs, far more than she’s made as an artist on Spotify with over 4 million monthly listeners. Today, companies like Royal and Sound facilitate NFT sales of limited copies of an artist’s new song, then help artists set up infrastructure around community interactions (both between fans themselves and with the artist). Sound has paid out 3.8 ETH (~$5k) to two artists in the first week of June 2022 alone, all while providing fans a more intimate relationship with their favorite musicians.

We agree with Adam’s point that “much in the crypto world was created and developed by idealistic, open-source developers and entrepreneurs with a desire to do good with their talent.” His main argument, though, is predicated on the entirety of crypto builders, holders, and users promoting and perpetuating subversive ideology that leads to social and political unrest and instability. In so doing, Adam applies a rubric to crypto that no other profound technological shift would survive. Indeed, this Fisher Test of Potential Subversity would have long ago felled many a paradigm shift including the supercomputer, online video, social media, online banking applications, the printing press, the wheel and fire.

Many of Adam’s arguments ring true as valid criticism but for more contemporaneous efforts to remediate. Jeff John Roberts outlines in great detail in Kings of Crypto Coinbase’s maniacal focus on staying above board with regulators, which was out of vogue at the time with the general sentiment of the ultra crypto-native, and the great lengths to which the company went to prevent fraud from being facilitated through the exchange. Even more specifically, Adam claims the “anarcho-libertarian ethos of Bitcoin permeates much of the broader crypto market.” Clearly, the reputational residue of the space’s most extreme purists has left an unsightly stain. But it doesn’t have to be this way.

One of Adam’s fundamental arguments seems to be that crypto by its very nature is “too volatile to be a currency like the dollar, too high maintenance to be a store of value like gold, and unlike a stock, crypto is also not a financial asset with intrinsic value.” We agree in principle with some—but not all—of these critiques but even if we grant them all, it does not necessarily follow from the lack of a historical analogue that the whole category is without utility. In fact, we see as profound the innovation that ownership of an asset—be it a currency, token or other digital apparition–is conferred at the protocol level via a distributed consensus mechanism where no one person, company, organization, or cabal controls the database that confers said ownership. This is a very powerful concept which will inevitably lead to the democratization of control of our most contentious asset, our own data—and give all of us more granular control of what the big tech companies (or any counterparty for that matter) know about us - and what they can do with that knowledge as a result.

Developer activity

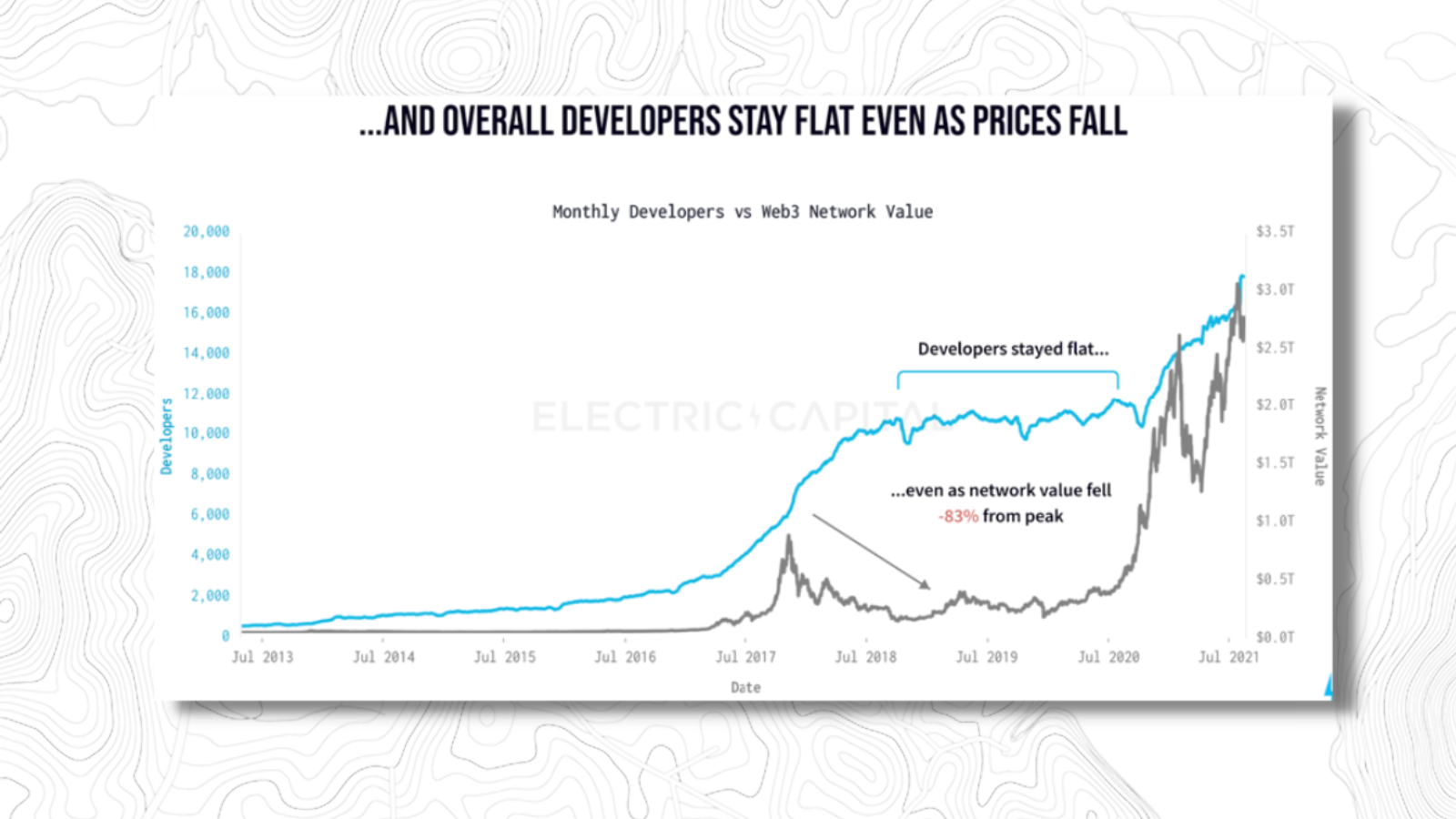

We believe the biggest counterpoint to general crypto naysayers can be found in the data around founder and developer activity. According to Electric Capital’s 2021 Developer Report, web3 developers are at an all-time high and growing faster than ever. In 2021, 18K+ monthly active developers committed code in open-source crypto and web3 projects, with 34K+ new developers committing code that year, the highest in history. Most interestingly, the overall number of developers stayed flat even as prices fell, suggesting that while newfound interest may initially be driven by speculation, there is a genuine commitment to the category that remains even when the tides run out.

As just one example, gaming has emerged as the perfect initial use case for crypto—as was also the case with the smartphone. Tony Sheng, co-founder of Cozy Finance, is one of the earliest writers we’ve followed on this trend and in a 2018 blog post distills succinctly how gaming faces problems of “liquidity, ownership, and scarcity—perfect problems for crypto to solve.” Digital ownership reduces the barrier to entry for players to try new games (e.g., players know they can sell their assets in a presumably liquid market if they no longer want to play), and addresses common player complaints focused on an inability to move assets from one account to another, buy assets that aren’t actively for sale in the primary markets, and general monopolistic control over supply (e.g., of a rare item) by game developers.

The years between 2018-2021 unveiled what we refer to as “v1” of crypto games, which we believe are really DeFi protocols with a thin game skin. We believe the next iteration of innovation is happening now, with monetization mechanisms becoming more than just a function of inflation and selling dynamics, but from increasing contract and ecosystem value through increased usage and trades between players. To be sure—and this has been largely missing from v1—the games need to be fun to play and the inclusion of crypto does not obviate the need for tried and true F2P gaming playbooks. To date, early efforts to bring crypto into gaming have locked out a large part of the population by requiring high upfront costs to purchase assets necessary to play the game. As talented artists, designers, and game producers continue to leave AAA studios to build web3 equivalents, it feels increasingly obvious that mass adoption will happen once they can “find the fun, reduce the pain, and overcome distribution challenges.” There are a few games already delivering on these premises and we fully expect more to come. Our current portfolio companies building in the space include Sorare, TSM, Wildlife Studios, Genopets, and a stealth seed investment.

While the crypto space comes with its fair share of hyperbole, beneath the hype we see a through line: we're optimistic in the blockchain's potential to allow developers to build their applications in a radically different way—without any one entity controlling the data. While some may believe it may be impossible to separate the speculative, “get rich quick” type of activity from the core innovation, our focus is on what we see to be tangible improvements to the existing system while recognizing the resiliency of our traditional institutions.

It’s not hyperbole to say there’s no other way to separate the application from the data in such a manner and this feels to us like a step function continuation of the API-ification of modern computing applications— where many companies have opened up access to their applications and databases for others to access (albeit in a controlled manner). Taking this next step as to where the data lives in the system—at the protocol level—doesn’t necessarily have to come with subversive intent.

These characteristics—permissionless, self-sovereign data and instantaneous value transfer—turn out to be key to the stark bifurcation of solvency between centralized and decentralized exchanges. True DEXs are continuing to maintain transaction volume through this downturn while their centralized counterparts are imploding. Though these models are yet to be capital efficient (over-collateralized lending is direct function of an ability to underwrite on chain today), they do fulfill the promise of lower transaction costs and facilitate payments that are 24/7, global, anonymous and allow participants to extract a piece of the value that they are bringing to the venue.

Ownership concentration

The pervasive view that BTC ownership is highly concentrated neglects a more nuanced evaluation of the evolving wallet landscape. In a research study cited later in our colleague’s piece supporting the concentration of BTC mining activity, the authors also scrutinize wallet addresses holding at least 1,000 bitcoins as of December 31, 2020. The fact that so few addresses control almost half of the BTC in circulation is often taken as prima facie evidence of the high concentration of Bitcoin holdings. This view, however, fails to recognize that not all Bitcoin addresses should be treated equal (e.g., an exchange address holding funds of millions of users needs to be distinguished from an individual’s self-custody address and some of these addresses belong to cold wallets and therefore, represent holdings of a large number of people). Headline statistics also fail to account for public and private companies holding crypto, new Bitcoin ETFs, payment processors (e.g., BitPay), crowdsourced wallets, and family offices. In fact, Bitcoin ownership has seen a dispersion over the years, particularly as institutional investors enter the space:

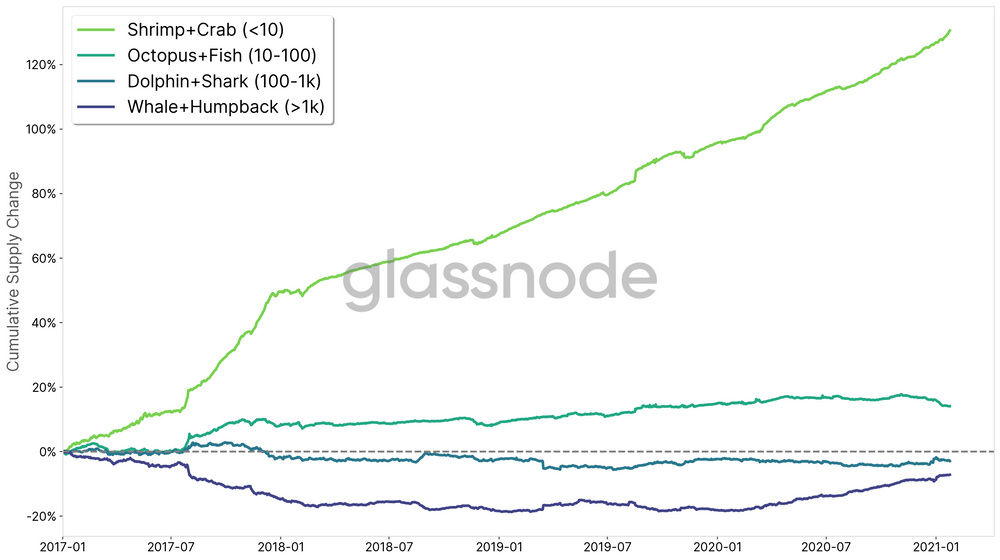

Per Glassnode's research (published in mid-2021), “whales” (1k-5k BTC) and “humpbacks” (>5k BTC) together control ~31% of the BTC supply, representing institutions, custodians, OTC desks, and others. However, the study also examines the “relative change in supply across these entity sizes” with the smallest entities (shrimps and crabs) increasing their holdings by 130% since 2017 and at 5% and 9% collectively, they are not insignificant. At the same time, large entities (dolphins, sharks, whales, and humpbacks) have decreased their BTC ownership by 3% and 7%, respectively:

Regulation

Lastly, we agree that regulation of crypto is needed for both protection of consumers and discouraging talent and innovation from seeking refuge offshore. As Gilad Edelman writes, “Law, with all its faults, is still pretty much the most effective technology ever devised for preventing people and corporations from abusing their power—and forcing them to share it.” However, in future crypto regulation, we don’t see a coming apocalypse or battle of the ideologues where the anarchists abscond with their crypto to a mythical seasteading-compliant island in the sea, but instead see government intervention as the beginning of the category going mainstream—conferring more and more legitimacy on the projects that embrace the crypto building blocks to build software in a uniquely improved way. And despite lobbying efforts—the likes of which exist across all industries—there is no sign that the coming regulation will be “light”; quite the contrary, there are efforts underway to bring myriad protections to the space that protect consumers from the kind of obvious and foreseeable failures which have been all too prevalent to date. This is no different than the kinds of regulatory actions taken in the wake of past TradFi meltdowns like the financial crisis of 2008 and the 1989 junk bond crash.

As we’re finding out in real-time, crypto isn’t yet a mature enough technology to have achieved a level of anti-fragility and resilience such that all of the many possible DeFi applications are workable today. But this same characteristic of fragility could be applied to many novel innovations writ large. Compare the recent depeg of the Terra/Luna linked algorithmic stablecoin to the mortgage-backed securities crisis of 2008. The former saw a large drawdown in crypto assets and a steep downturn in the price of BTC and ETH (though a trajectory already in motion prior to the depeg in conjunction with public and private equity markets), impairing the value of most other altcoins. But the system survived and where traders previously relied on UST as a base pair, they substituted an alternative.

In contrast, the pervasive securitization and packaging of tenuous mortgage-backed securities could very well have brought down the entire global financial system as we know it—absent a massive government bailout program that had the Fed injecting up to $700 billion directly onto the balance sheets of such venerable bastions of stability as Goldman Sachs, AIG, and Morgan Stanley. None of them would have survived otherwise. And so, while cryptocurrency cycles are profound and many currencies have outright vanished overnight, the system has survived and with each failure evolved for the better.

Moreover, Adam also mentions that DAOs have done little to promote democracy in the name of decentralization. While there is also quite a bit of innovation in furtherance of these ideals (quadratic voting comes to mind), fundamentally the expressed purpose of DAOs is not to curb bad actors. Instead, we believe they uniquely reduce friction in crowdfunding small dollar amounts from a large quantity of participants, resulting in influential capital pools that can be designated towards a number of ends, including collecting and investing.

We feel confident that while it will be messy, crypto will follow the same general pattern of regulatory efforts as many new innovations. Take social media, which emerged with the advent of Friendster and Myspace in the early 2000s. Despite the better part of two decades as a test run, regulators are still struggling to catch up and protect the consumer from the harms that products like Facebook, Instagram, Twitter and TikTok have been shown to cause. While some might wish to relegate this entire category to the dustbin of history, we feel strongly that the solution—to all new technological capabilities—is proactive and sensible regulation, not banishment. The Biden Administration gets this as well and has been proactive about issuing orders calling for responsible development of digital assets to protect consumers and the financial system without sacrificing the potential good inherent in the system.

Crypto: Neither good, nor bad, nor neutral

We conclude with where we started - respect for the sounding of an alarm about the potential perils of a technological innovation with the potential to evolve into a quasi-political movement. But while our respected colleague sees a “sweeping reorganization of our imperfect…economic system” and views proponents as “evad[ing] moral culpability of any negative externalities that occur,” we are far more hopeful. With the blockchain, we see a system proving itself to be resilient and multi-faceted. We see a reckoning between projects and companies with little novelty in product development but for speculation-oriented tokenomic designs getting crushed quickly in favor of more stable projects with less explosive rocketship potential but more lasting and fundamental utility. And in mainstream developers and founders choosing to build blockchain-based applications, we have tremendous faith that the nefarious actors will quickly be watered down by the same forces of good that (usually) keep our democracies stable and economic world order functioning. Developers serve as yet another check on possible subversive outcomes, and in the process make it that much harder for any sect of crypto overlords to implement the kind of new-age feudal system Adam fears. It certainly helps to go in eyes wide open to the promises—and also the perils—of any new technological advance. But just as the internet, social media, and artificial intelligence are all double-edged swords, we see in the advent of blockchain-based applications the same dichotomy. And we continue to possess the audacity to believe that the existing world order can accommodate this potential disruption all the same.

Building in the space? Please reach out to Ethan Kurzweil, Lindsey Li or any member of the crypto team (crypto@bvp.com). Want to join the discussion? Jump in on Twitter or on the BesssemerDAO Discord.