Roadmap: Reinventing life sciences with AI

As the global life sciences industry aims to manage costs and accelerate launches, AI is rewriting how services and software are delivered.

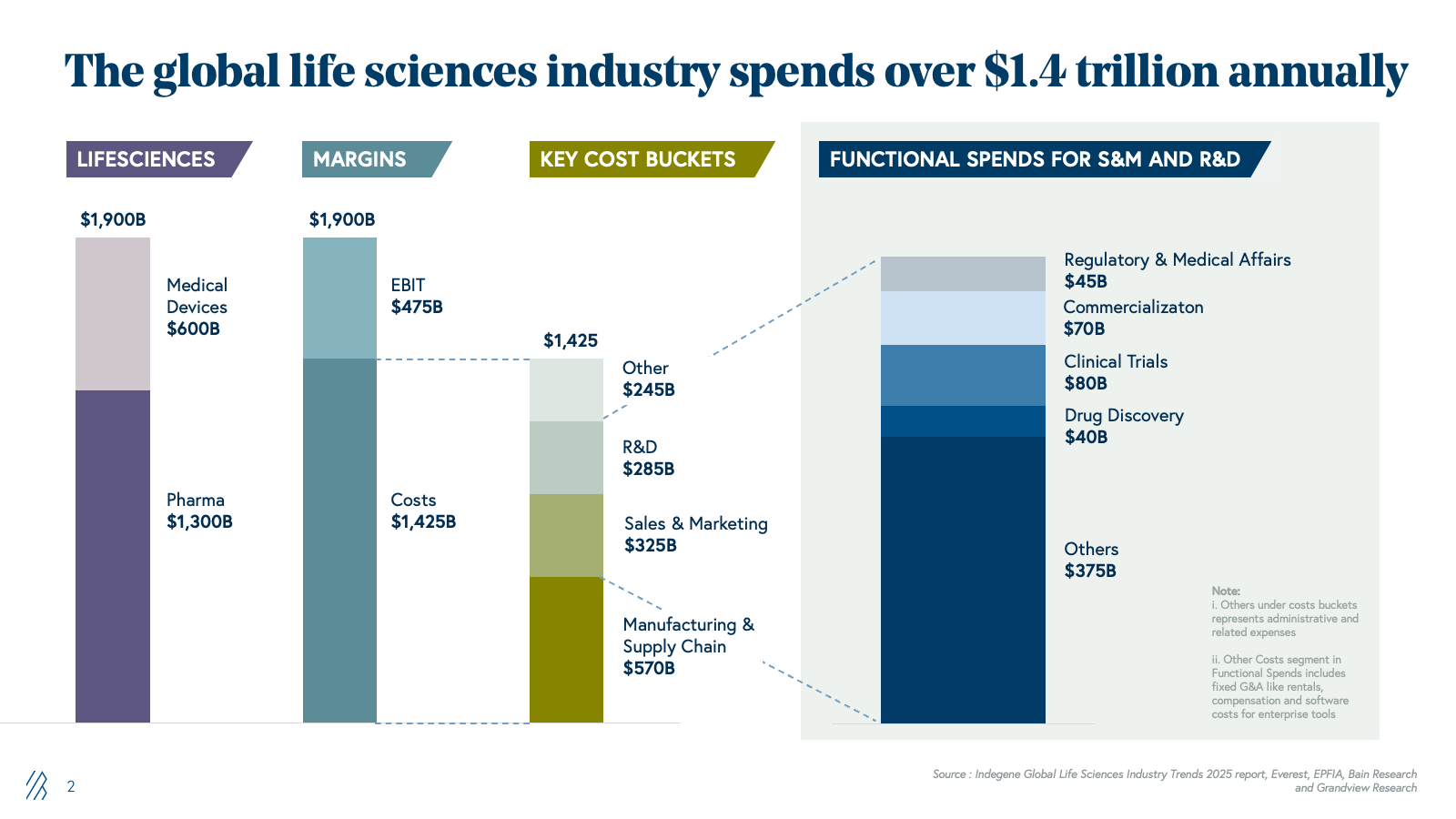

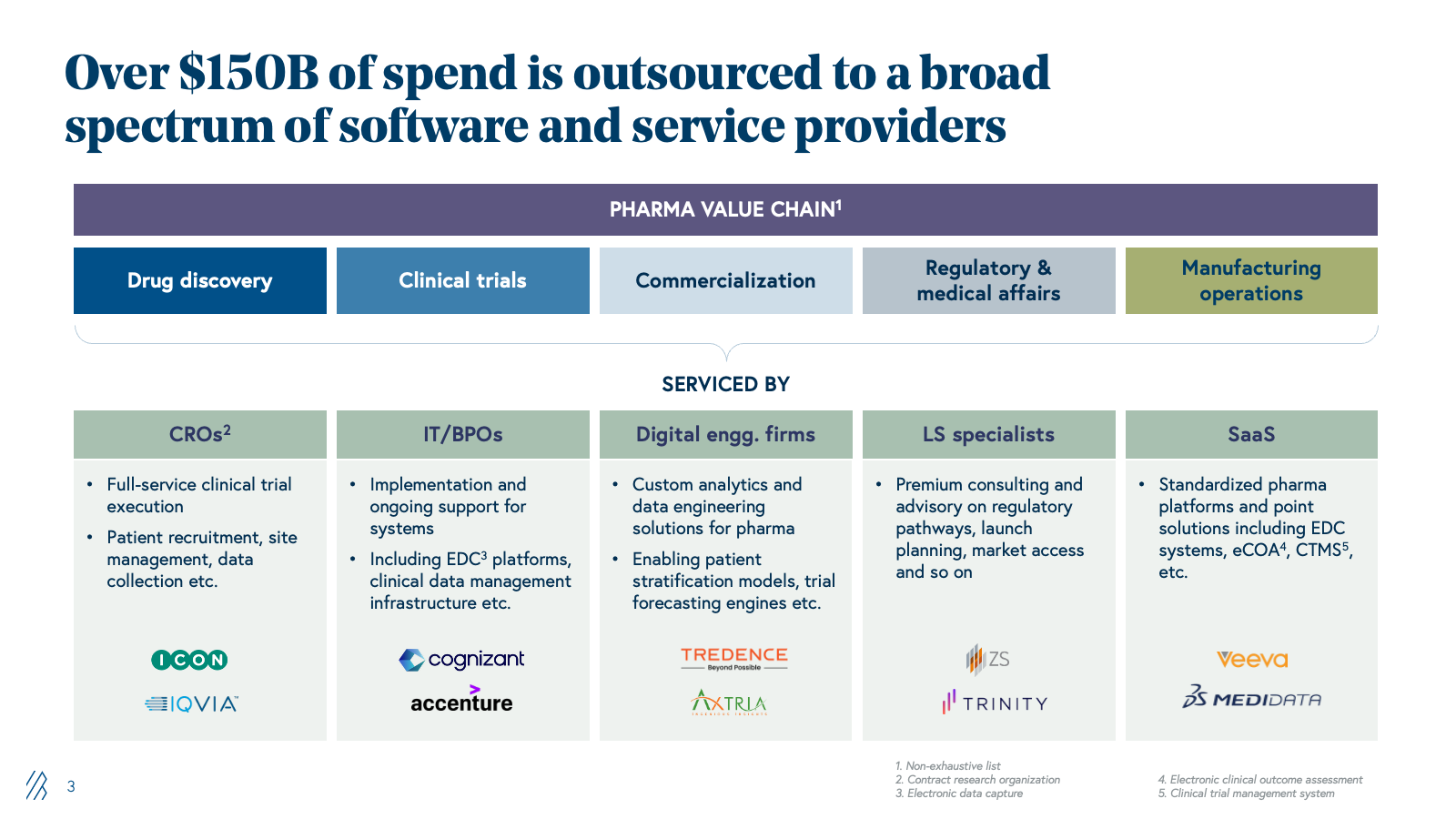

Pharmaceutical companies collectively spend over $150 billion across service providers and software for drug discovery, clinical trials, operations, regulatory affairs, and commercialization. Incumbents have historically built upon three core pillars:

- Deep domain expertise (PhDs, clinicians, regulatory specialists)

- Access to large global talent pools (often offshore)

- Hands-on coordination of complex, end-to-end workflows

Now, the expertise-and-people-driven model that defined outsourcing is being rewritten by AI agents that automate workflows across the value chain. This disruption is generating a new wave of AI-native challengers- startups pairing domain scientists and engineers with proprietary AI platforms to deliver faster, cheaper, and often higher-quality outcomes than incumbents.

Our roadmap addresses these changes with AI surrounding pharma and life sciences outsourcing, including the addressable opportunity and value AI can unlock, why adoption remains stalled, incumbent vulnerabilities, and what next-generation solutions must offer to win.

We explore this disruption across five critical domains: drug discovery, clinical trials, commercialization, regulatory and medical affairs, and manufacturing operations, including the parallels from what we’ve witnessed across India's IT services sector.

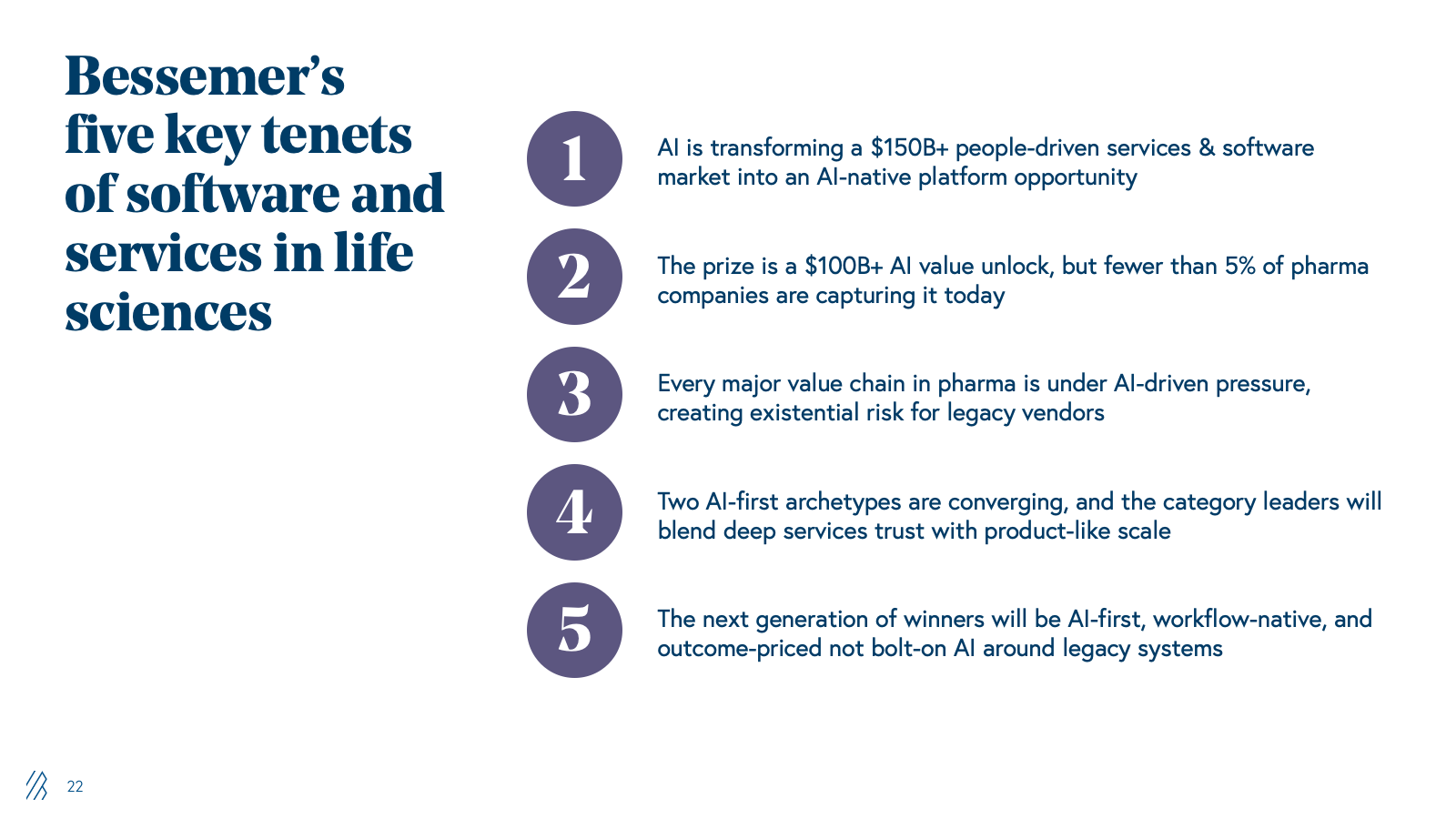

Key takeaways

- AI is transforming the $150B+ outsourced pharma and life sciences market by automating labor-intensive workflows across drug discovery, clinical trials, regulatory and medical affairs, commercialization, and manufacturing operations.

- Generative AI and agentic systems can unlock over $100B in net annual value by reducing costs, compressing timelines, and boosting revenues across the end-to-end pharma lifecycle.

- Despite the potential, only about 5% of pharma companies have captured measurable AI value due to legacy data silos, fragmented ownership, and vendor models built on billable headcount and seat-based licensing.

- AI-first challengers are emerging in two shapes- AI-integrated services and AI-native SaaS - both challenging incumbent CROs, consultants, and software vendors whose economics depend on manual work and long projects.

- The real competitive advantage will accrue to pharma companies and vendors that use AI as a unified capability layer to orchestrate workflows across discovery, development, manufacturing, and commercialization, rather than as isolated point tools.

Full slide deck

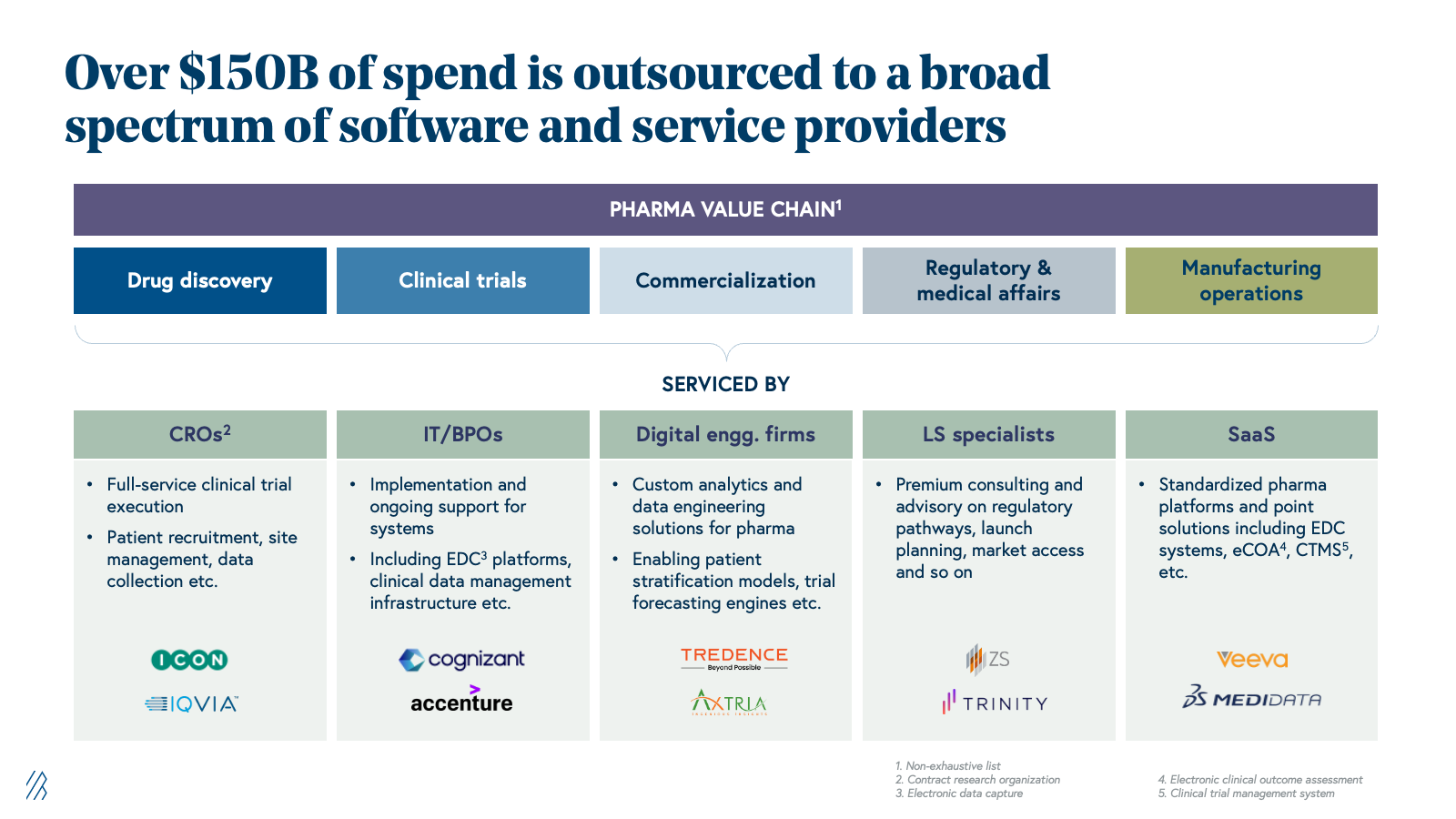

The installed base: $150B+ of outsourced work in pharma and life sciences

Pharma companies have systematically outsourced functions that were once core to their business operations in the past two decades. Now, they’re relying on specialized external partners to manage clinical trials, operations, regulatory submissions, and go-to-market strategy rather than maintain in-house teams for every capability. This shift in pharma companies reflects a simple economic reality: they don’t need deep expertise across every function when specialized, vendor-driven models can deliver better outcomes at a lower cost.

This outsourcing trend has since matured into a $150+ billion addressable market. Contract research organizations (CROs) now handle the majority of clinical trials globally, regulatory and medical affairs services span submissions through pharmacovigilance and commercial support, and specialized providers handle market access, pricing strategy, and field force optimization.

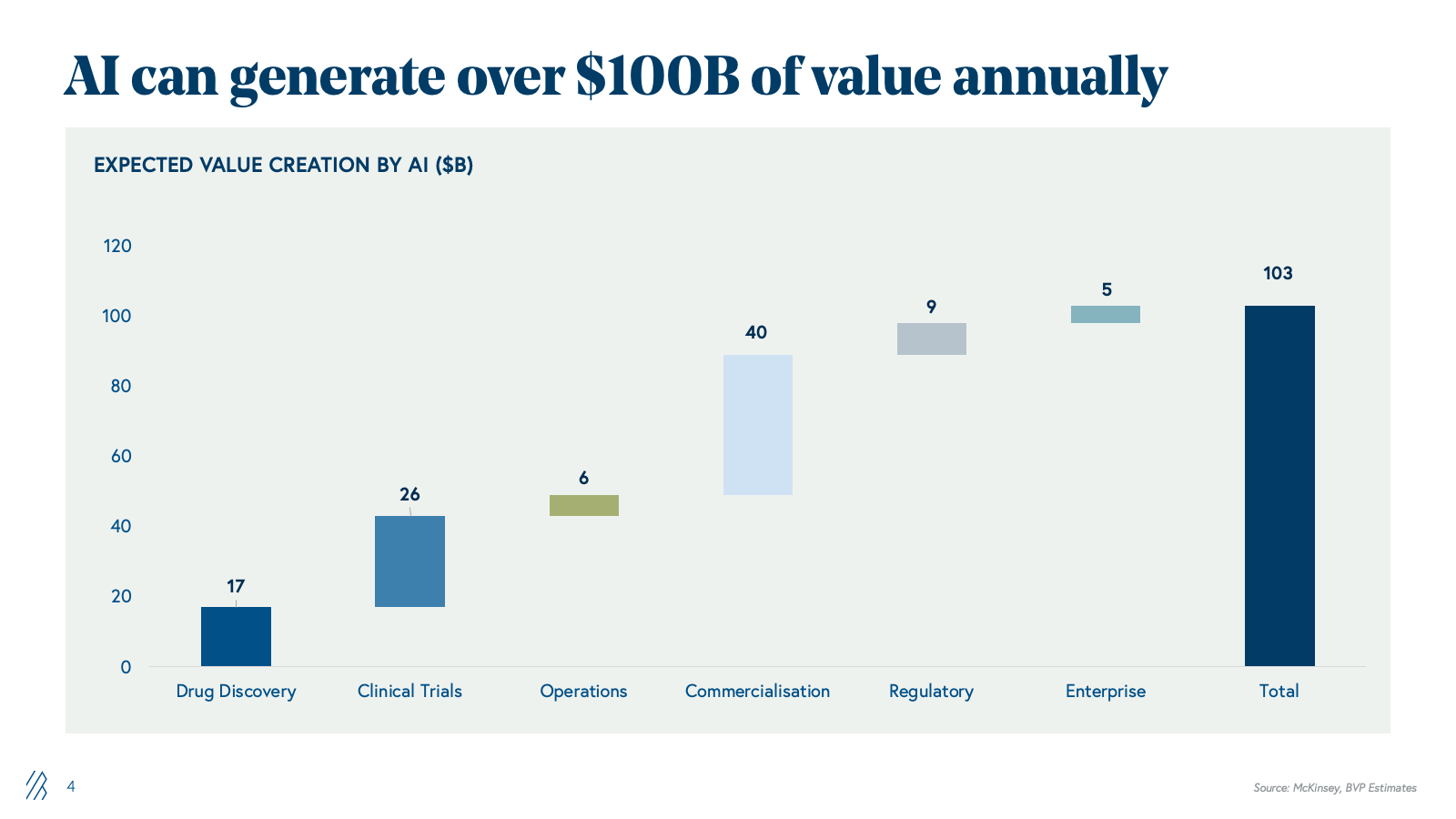

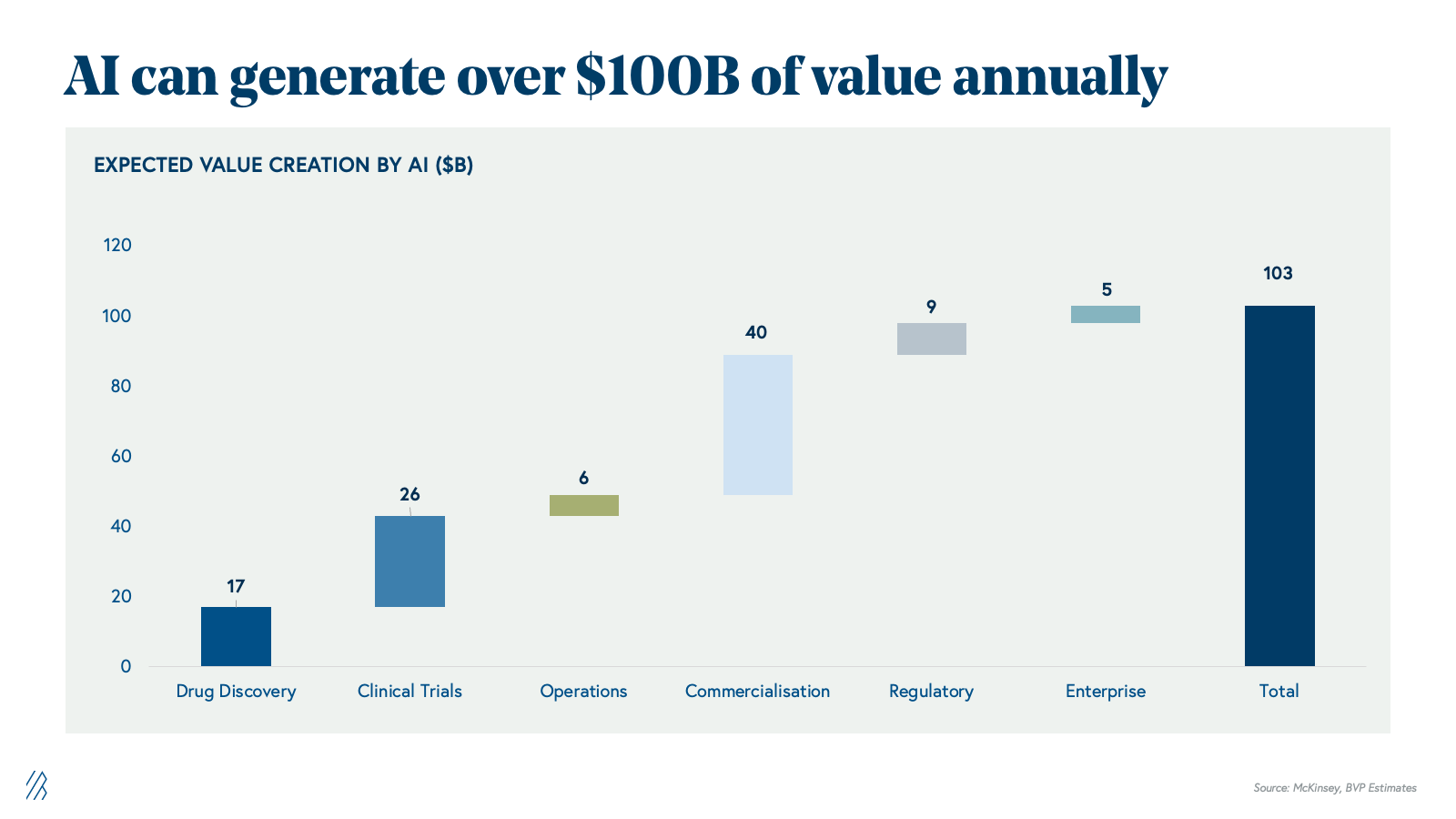

The AI opportunity: $100 billion in value unlock

The market’s inflection point is the convergence of two structural forces. First, global pharma faces mounting economic pressure to reduce time-to-market, compress costs, and maximize commercial returns. Second, technology readiness has advanced substantially; generative AI and agentic systems can now automate the knowledge-work and orchestrate the complex processes that have historically required large, cross-functional teams of specialized experts.

With AI, the industry can potentially unlock over $100 billion in annual value across the global life sciences value chain as an intelligence layer that compounds gains from discovery through commercialization. This $100B+ represents net economic value creation, and not a redistribution of the $150B+ currently spent on outsourced services and software. This additional value comes from three reinforcing levers:

- Cost reductions: fewer failed programs, lower clinical and manufacturing spend, leaner SG&A

- Productivity gains: shorter cycle times, higher throughput per FTE, more programs advanced with the same headcount

- Incremental revenue: more successful launches, longer and higher peaks, better pricing, and access.

AI effectively expands the total economic pie by improving how discovery, development, manufacturing, and commercialization are executed, rather than merely reshuffling existing outsourcing budgets. This is showing up in tangible ways across the lifecycle.

In discovery, generative and predictive models accelerate target identification, de novo design, and lead optimization, shrinking cycle times and reducing the number of dead-end programs that consume R&D budgets. In clinical development, AI-driven patient stratification, biomarker discovery, and trial simulation improve protocol design and enrollment, raising the probability of technical and regulatory success while cutting avoidable trial costs. In manufacturing, AI optimizes expression systems, process parameters, and quality controls, increasing yields and reducing batch failures that quietly erode margins. On the commercial side, AI-powered forecasting, pricing, and access analytics, and market intelligence help teams capture first-mover advantages and maximize launch economics.

The real opportunity lies in recognizing that individual pharmaceutical companies that adopt AI as an end to end capability layer linking discovery insights to clinical strategy, manufacturing decisions, and go to market execution will gain disproportionate competitive advantage and capture an outsized share of this $100B opportunity, while those adopting AI only as isolated point tools will fall behind as the industry unlocks value through orchestrated, data driven workflows.

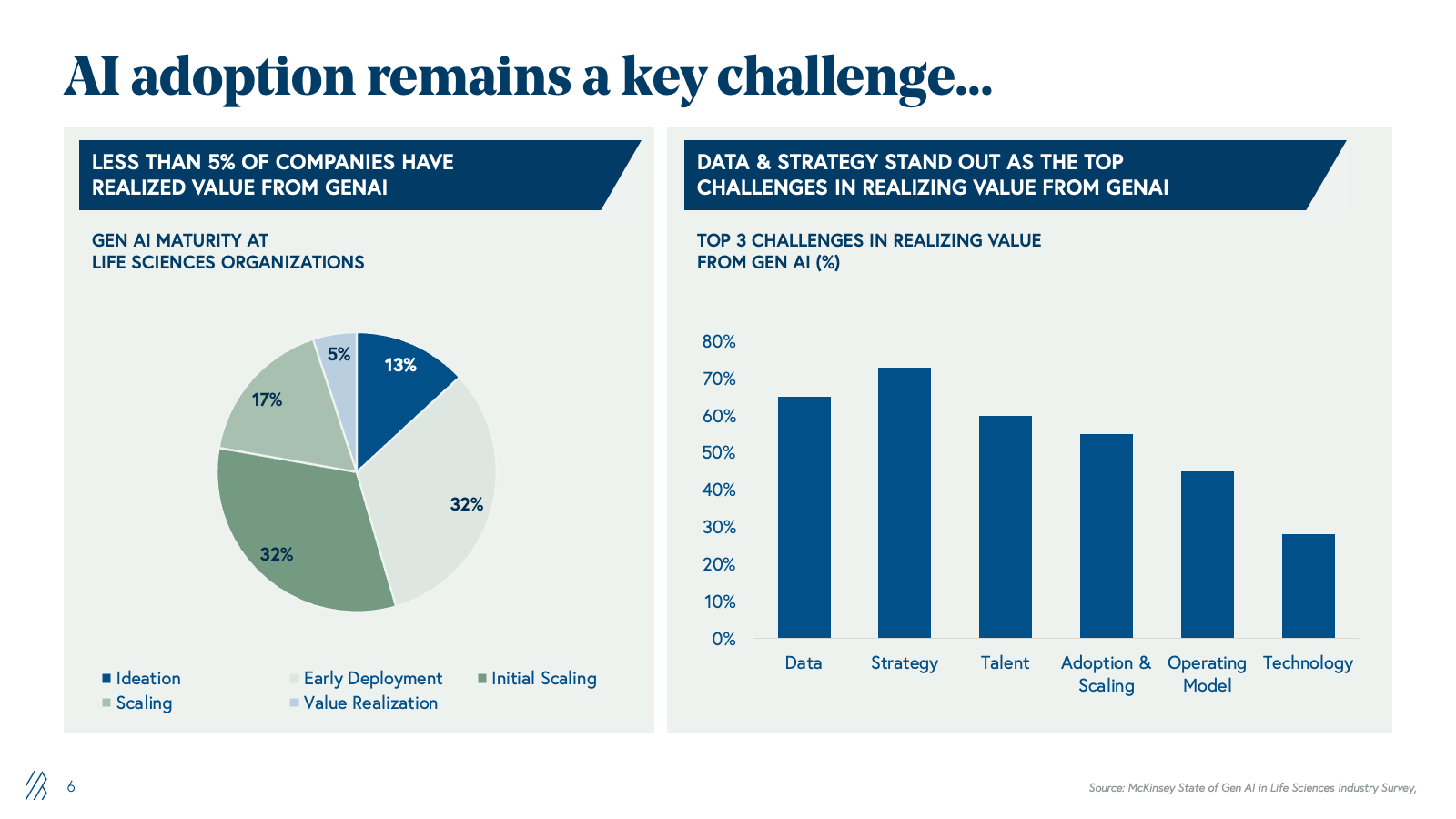

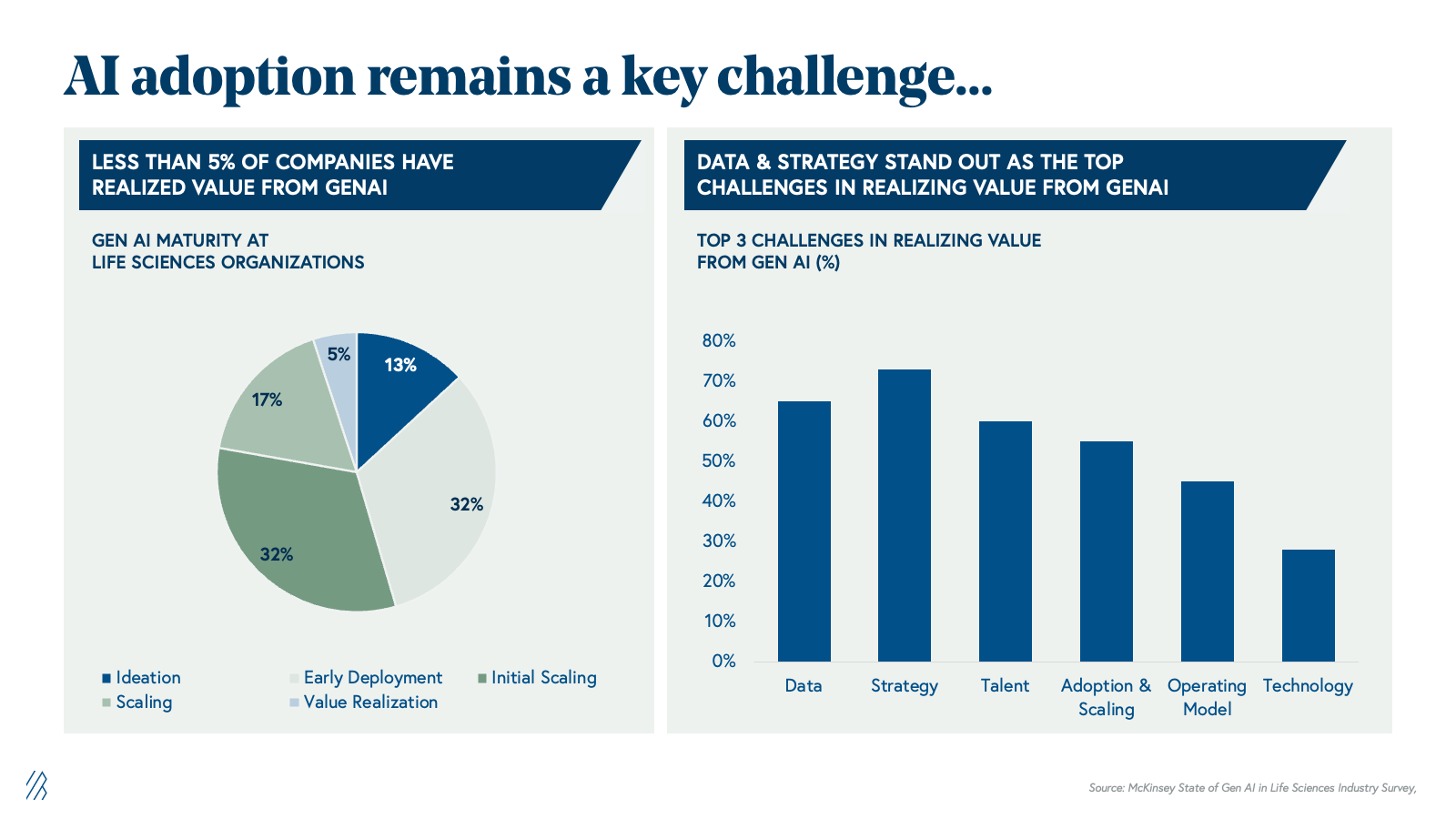

Why AI adoption remains a critical barrier: The 5% problem

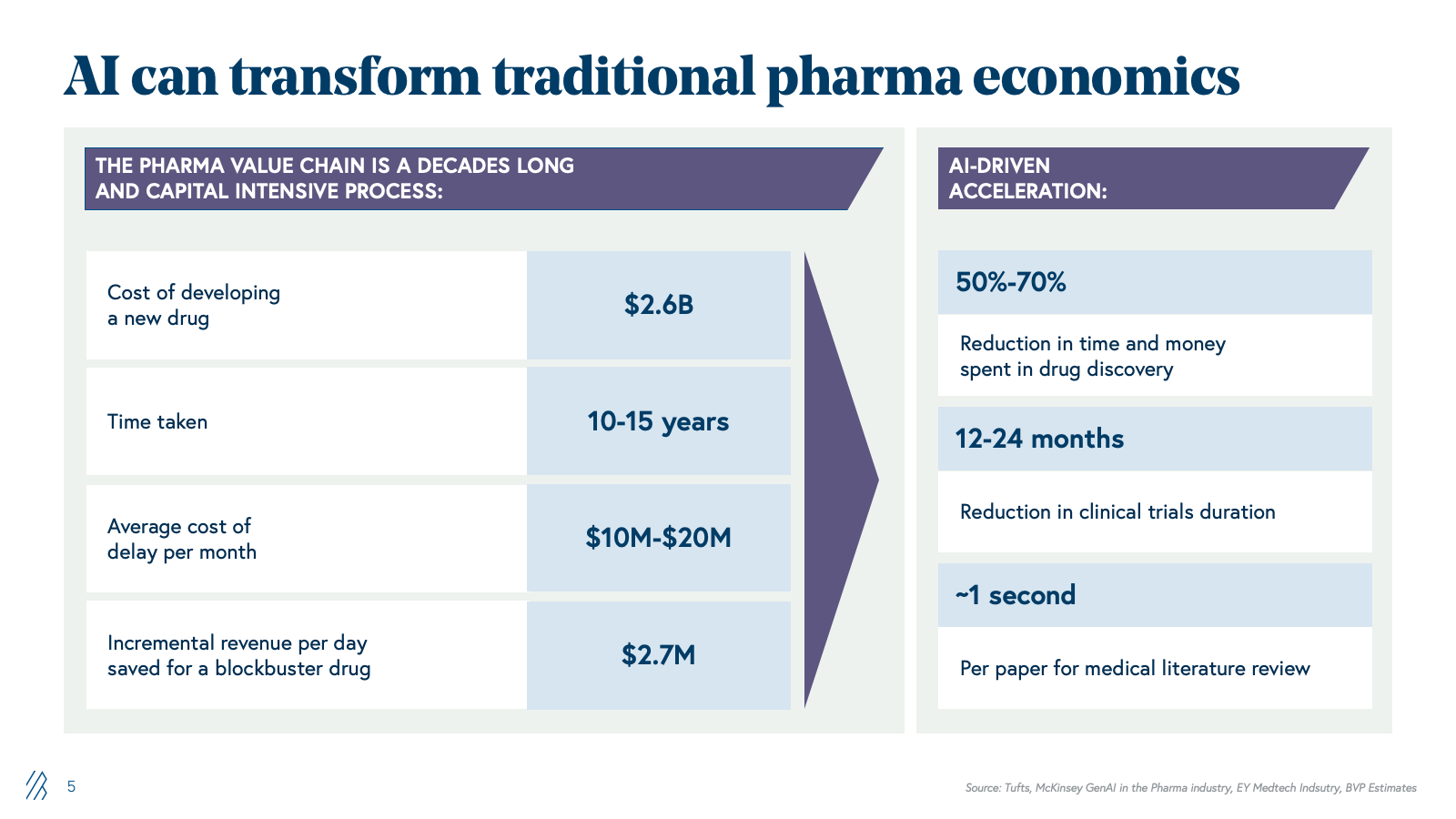

Despite substantial potential, only 5% of pharma companies have realized measurable value from generative AI. The barrier is not capability-driven; it's structural. Pharma's legacy infrastructure, built over decades, has resulted in data silos that are fundamentally misaligned with AI's requirements around data, strategy, talent, and operating models.

Consider the typical pharma landscape:

- Clinical data is captured in electronic data capture (EDC) systems optimized for regulatory submission, where it’s highly controlled and often difficult to operationalize for ML pipelines.

- Manufacturing data is trapped in historians and MES platforms optimized for batch records. Commercial data is scattered across CRMs, prescription databases, and incompatible dashboards. Regulatory submissions exist as PDFs and Word documents.

- AI initiatives are often owned by isolated teams with no clear mandate, underpowered data science groups, and inadequate governance frameworks to ensure value realization.

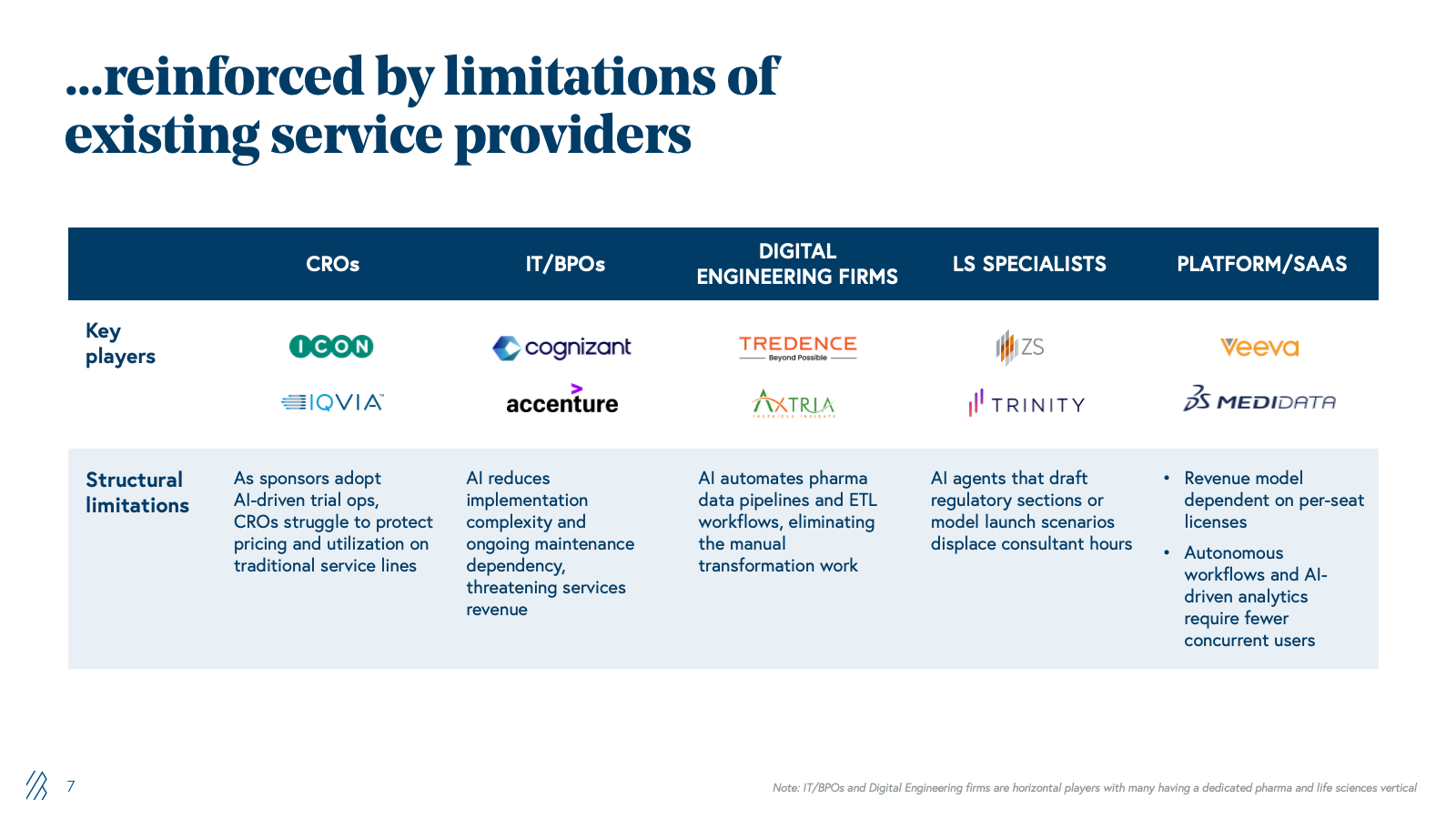

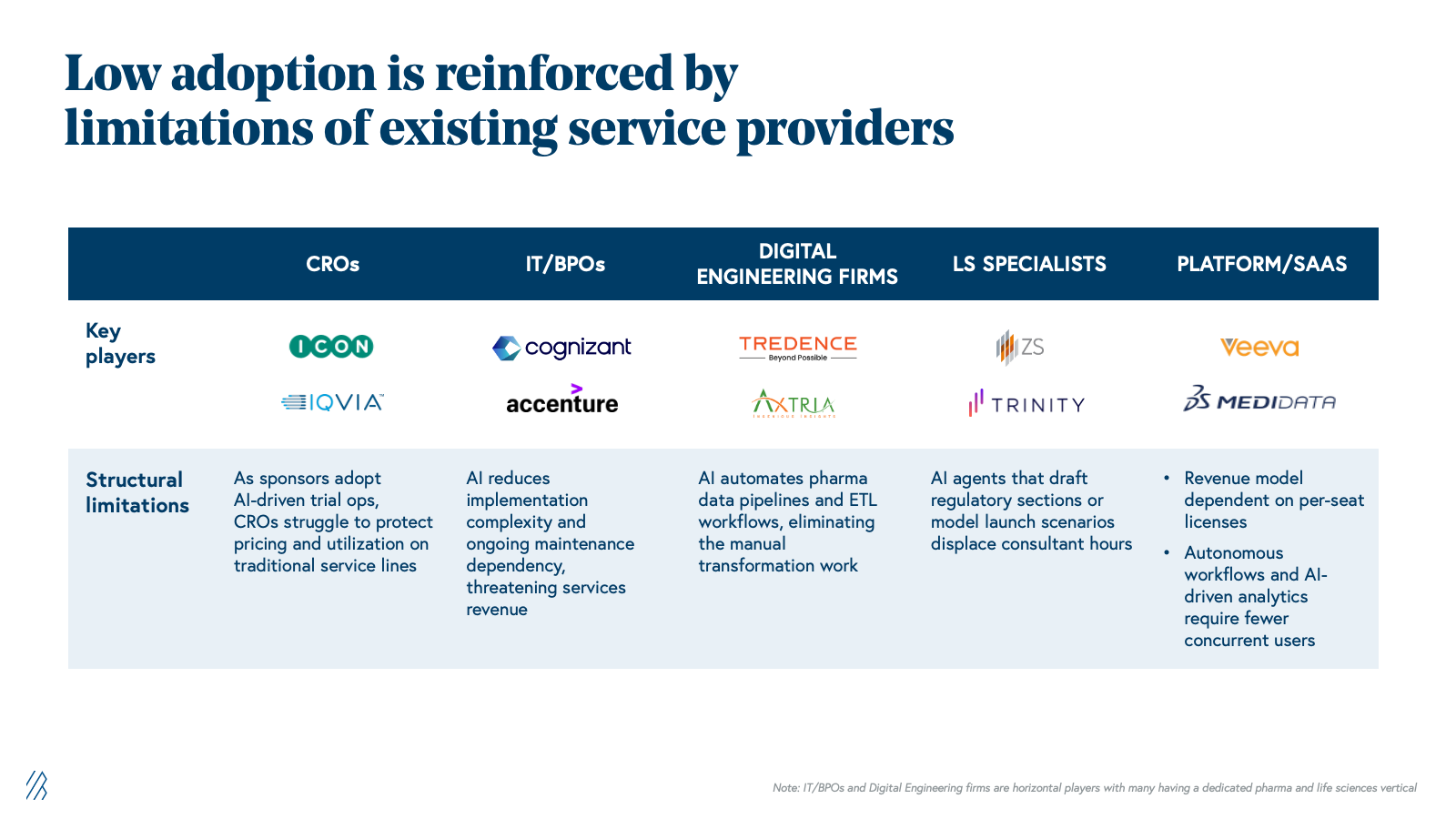

This adoption gap is reinforced by the vendor ecosystem. CROs derive margins from billable headcount, and automating workflows threatens their unit economics. IT providers that implemented Medidata and EDC systems charge for maintenance; AI reduces that dependency. Digital engineering firms like Tredence build custom analytics on top of legacy pharma systems, while they have been trying to productize their offerings, their DNA remains services-oriented. Consulting firms specializing in regulatory strategy and market access charge $300-500 per hour for guidance on NDA submissions and launch planning; AI agents that can draft regulatory sections or model competitive scenarios threaten senior consultant utilization. Platform vendors like Veeva rely on per-seat licensing; AI that reduces users is economically destructive. None are architected for AI-driven automation or outcome-based delivery. This is structural: vendor margins depend on labor, implementation, or seat counts, all of which AI directly threatens.

New entrants unencumbered by legacy systems can build AI-first service delivery models and target pharma companies ready for transformation. AI's impact spans the entire pharma value chain, and each domain faces distinct adoption barriers, unique incumbent vulnerabilities, and specific opportunities where AI-first providers can capture value at scale.

Five value chains under disruption

Major parts of the pharma value chain are under disruption by AI, changing processes and leaving incumbents vulnerable.

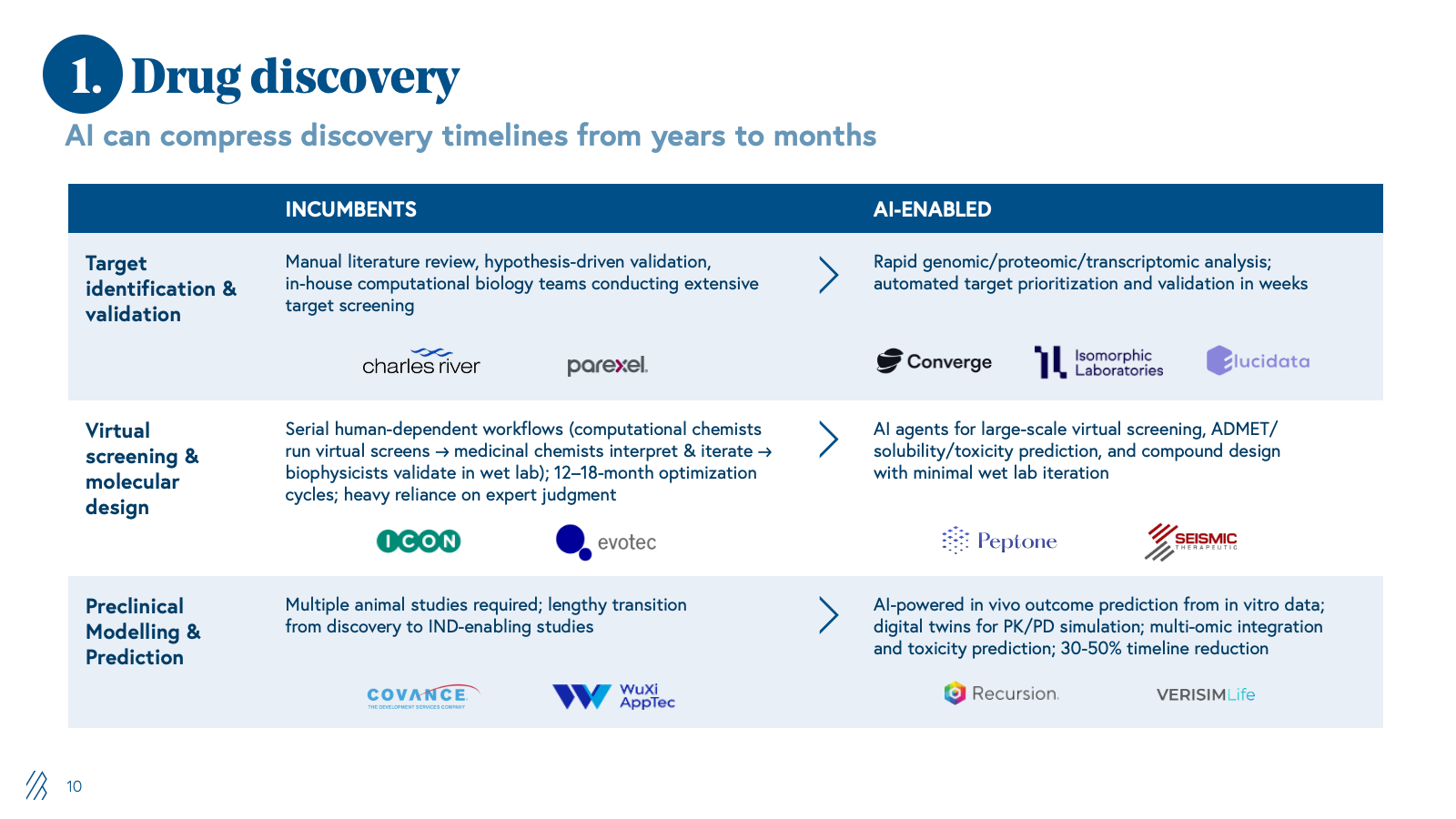

1. Drug discovery

Historically, drug discovery has been a slow, serial, experiment-heavy process. Internal R&D teams, supported by boutique CROs, have managed assay development, in vitro/in vivo work, and preclinical modelling as a largely sequential workflow dependent on expert judgment and iterative wet lab validation.

AI is reimagining this process by shifting from brute-force experimentation to computationally guided design. Foundation models for chemistry and biology now enable in silico target identification, de novo molecule generation, and virtual screening. This allows only the highest-value candidates to reach the wet lab, compressing timelines and reducing waste on dead-end compounds.

As value migrates from billable bench work to model-driven platforms, traditional discovery CROs built on FTE utilization and extended project timelines are structurally disadvantaged, while providers that treat AI as the core engine of a discovery service will define the new competitive benchmark.

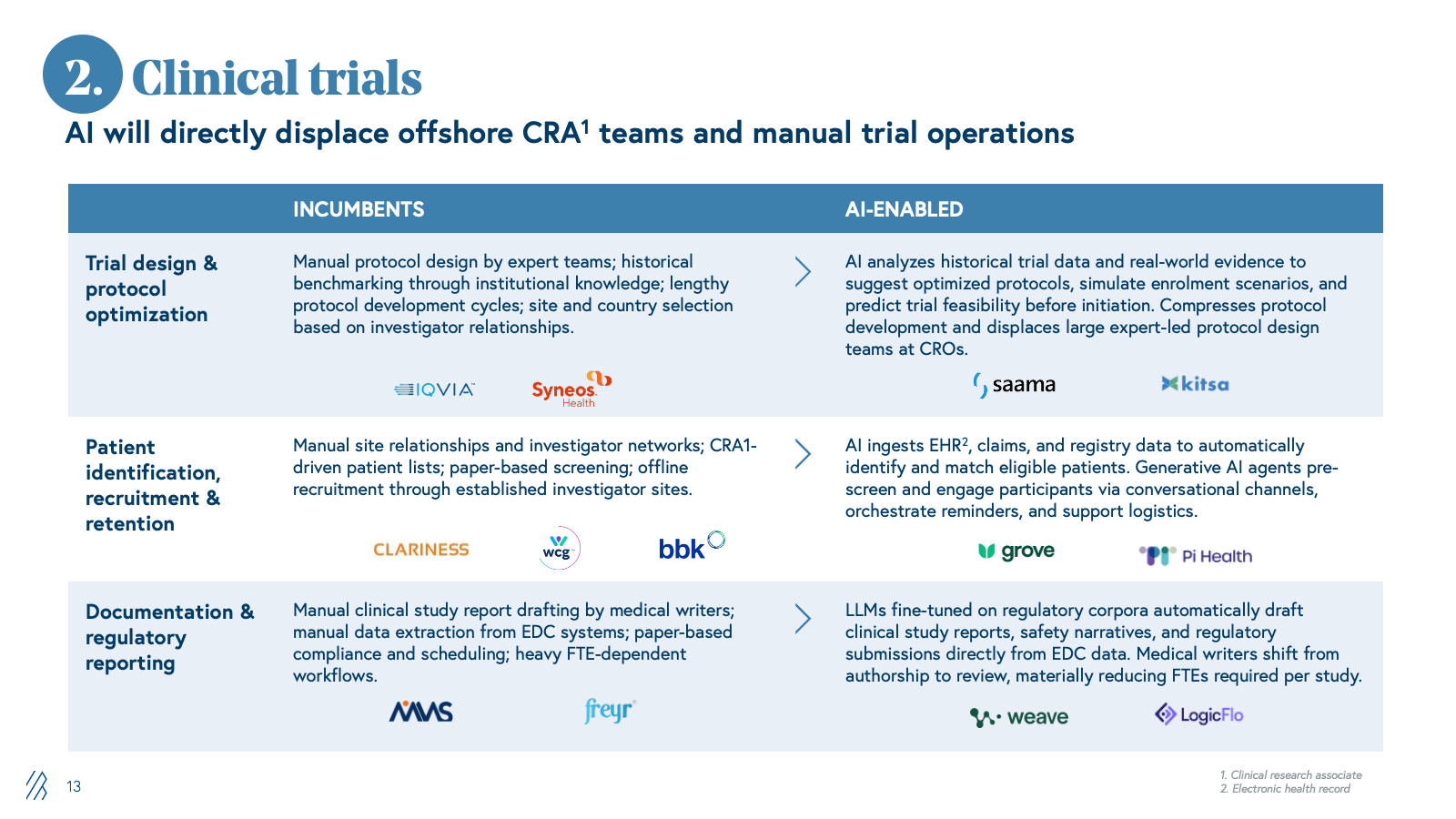

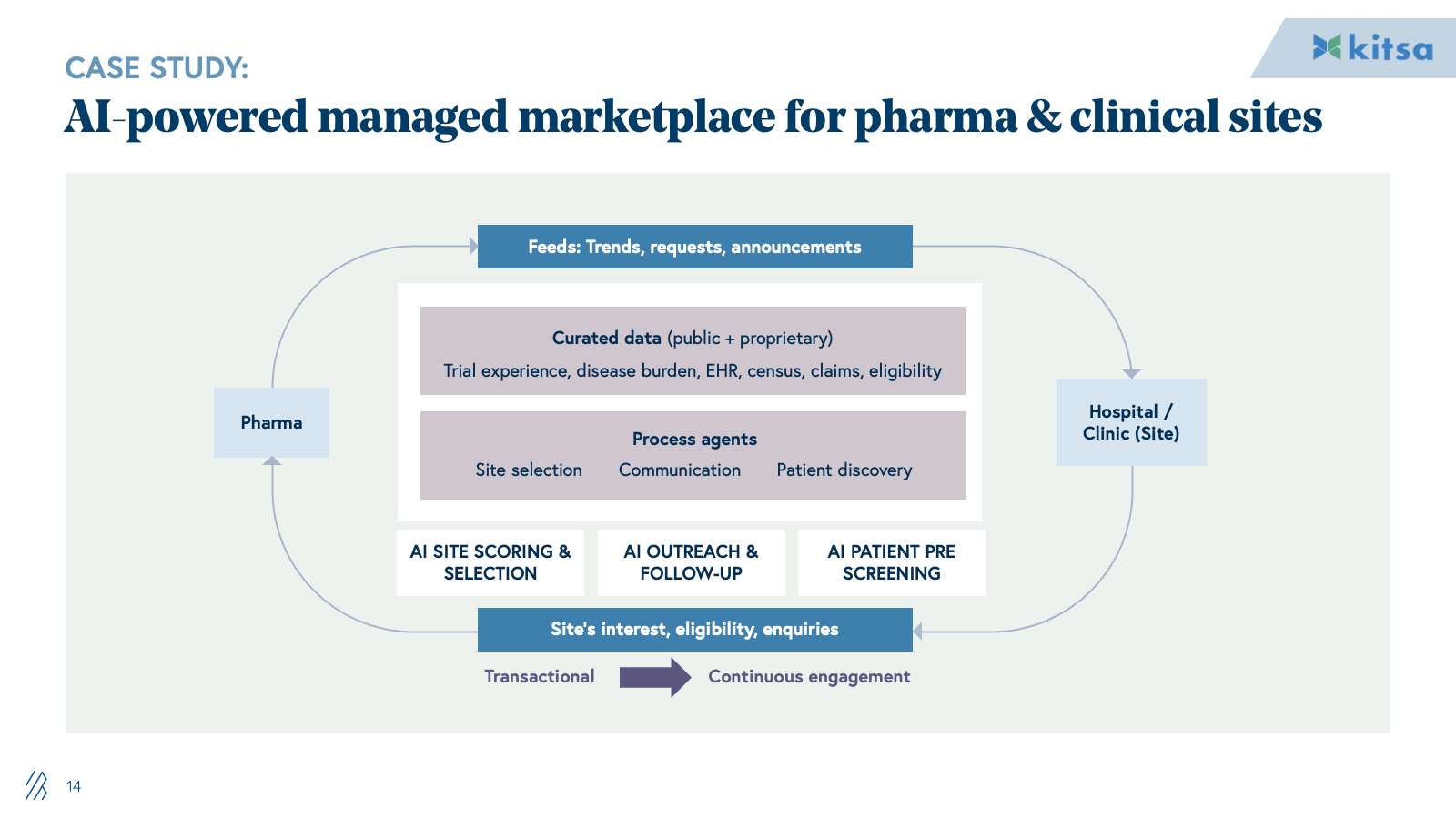

2. Clinical trials

CROs manage global trial activity from protocol design and site selection through recruitment, data management, and regulatory reporting. This is an operationally intensive model; large teams of clinical research associates, data managers, and medical writers manually coordinate sites, collect data, and prepare submissions.

AI automates the labor-intensive workflows that drive CRO margins. Patient identification and recruitment shift from manual site relationships to algorithmic matching against EHR and claims data. Protocol optimization moves from expert-led design to data-driven simulation of enrollment and feasibility. Documentation and regulatory reporting transition from manual drafting to LLM-assisted generation from EDC data. Medical writers shift from authorship to review.

This directly displaces the offshore and onshore CRA and data management teams that form the backbone of traditional CRO profitability. Providers who can deliver trial outcomes through AI-augmented teams will command dramatically different unit economics than incumbents, dependent on FTE scaling.

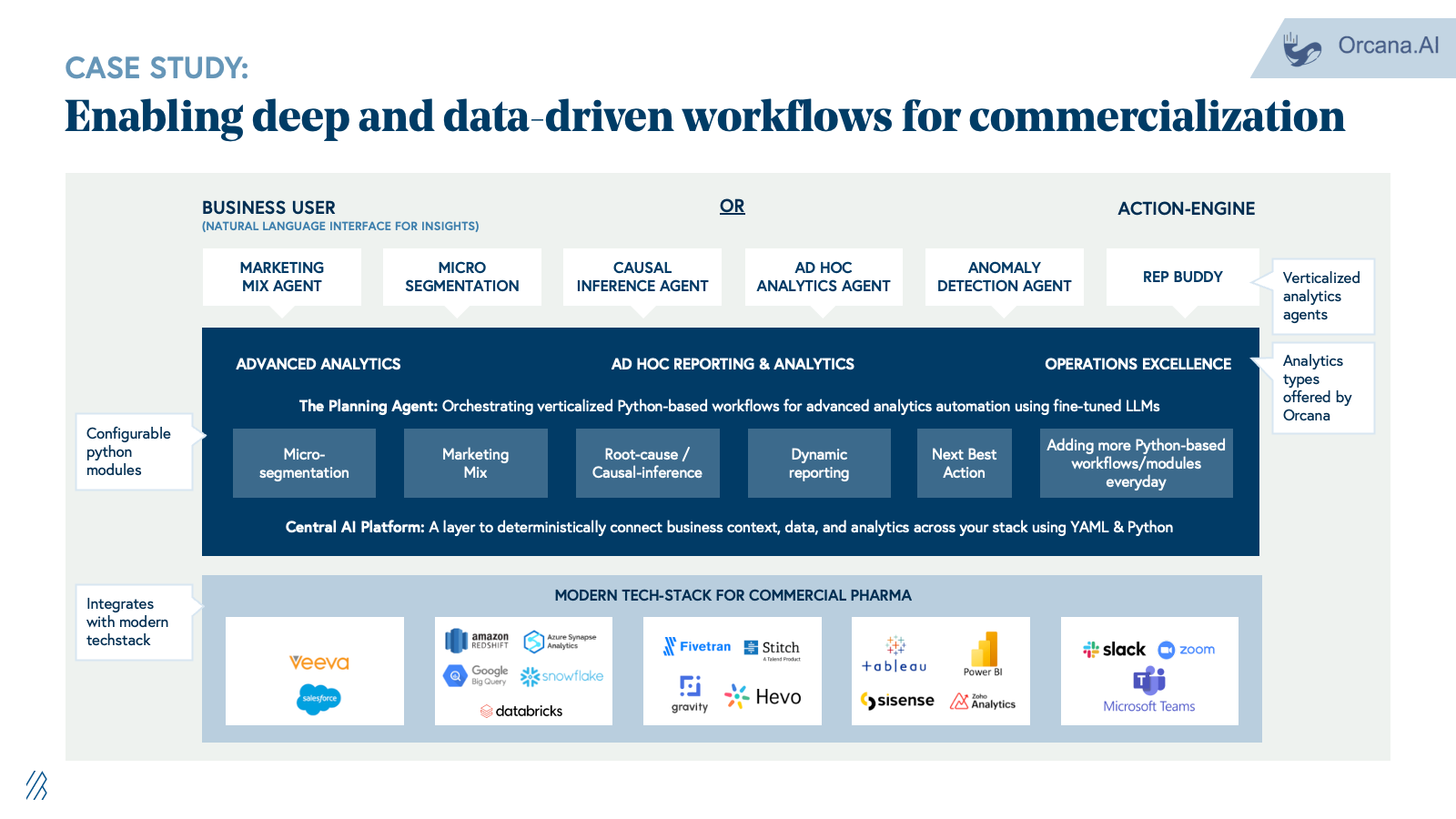

3. Commercialization and market access

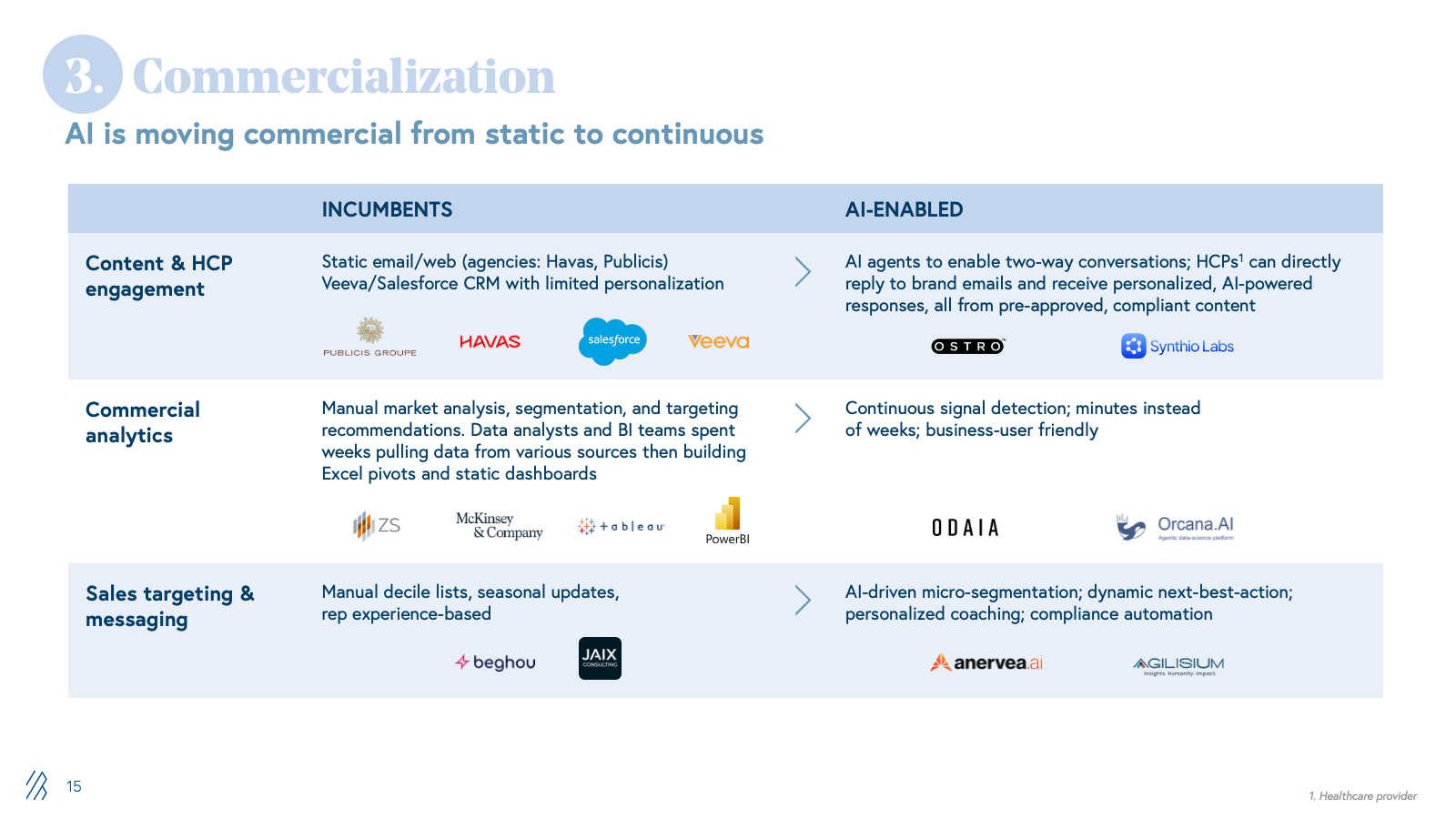

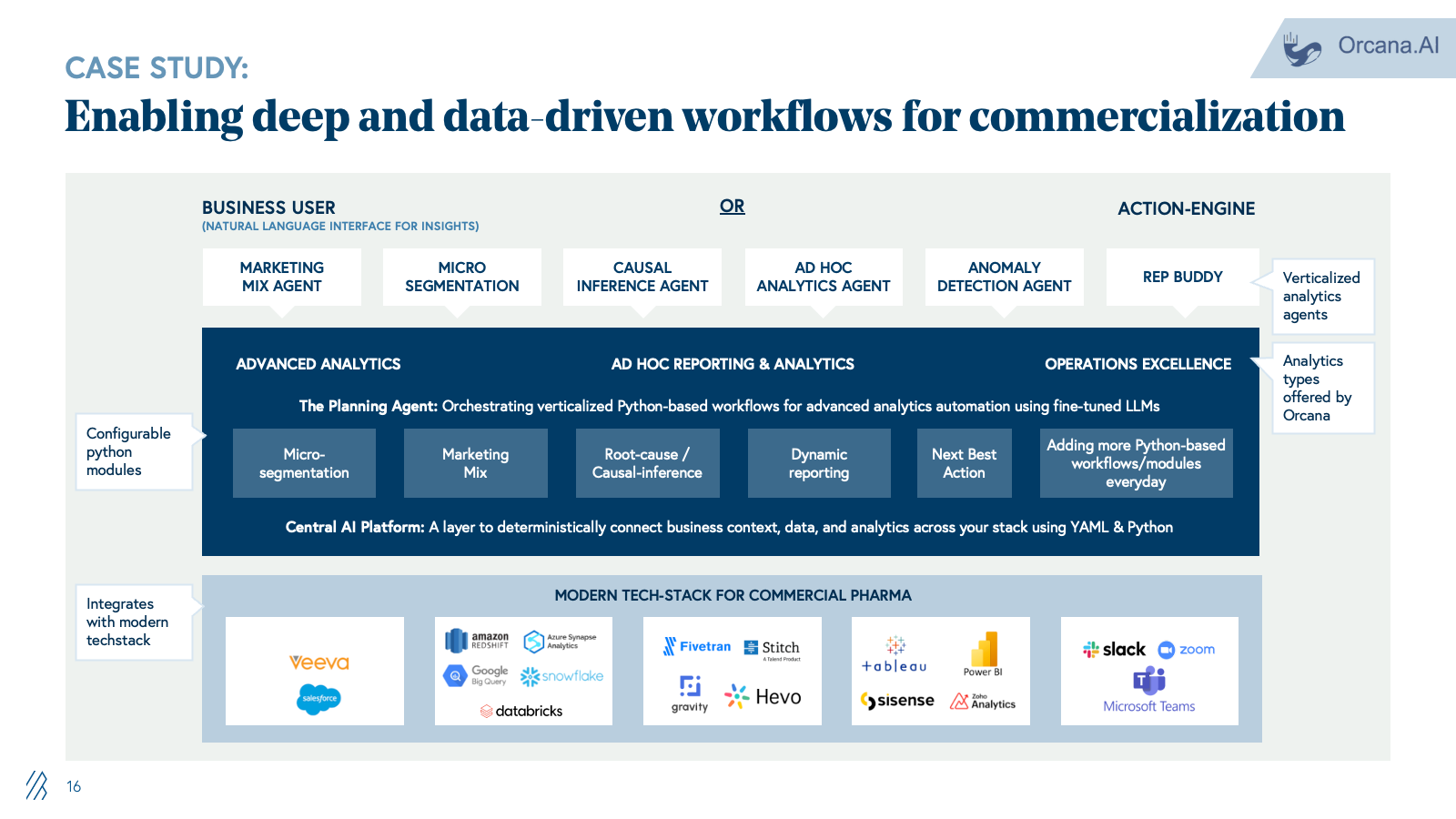

Commercialization is supported by consulting firms, market research firms, LS-focused agencies, and field force outsourcing providers handling launch strategy, segmentation, message development, campaign execution, and sales enablement. Work is largely project-based with deliverables relying on static decks, dashboards, and content libraries.

AI shifts commercialization from static planning to dynamic execution. Content engagement moves from generic campaign blasts to real-time, personalized HCP interactions powered by AI agents trained on compliant content libraries. Commercial analytics transition from manual data pulls and Excel pivots to continuous, AI-driven micro-segmentation and next-best-action recommendations updated daily. Sales targeting evolves from static quarterly plans to dynamic territory orchestration that adapts targeting, messaging, and materials based on real-time performance data.

This disintermediates traditional consultancies and agencies. When companies can log into a system that recommends HCP priorities and auto-generates compliant content variants, the appetite for long strategy engagements and manual campaign management collapses. Providers who deliver execution velocity through AI will outcompete those selling labor-intensive advisory services.

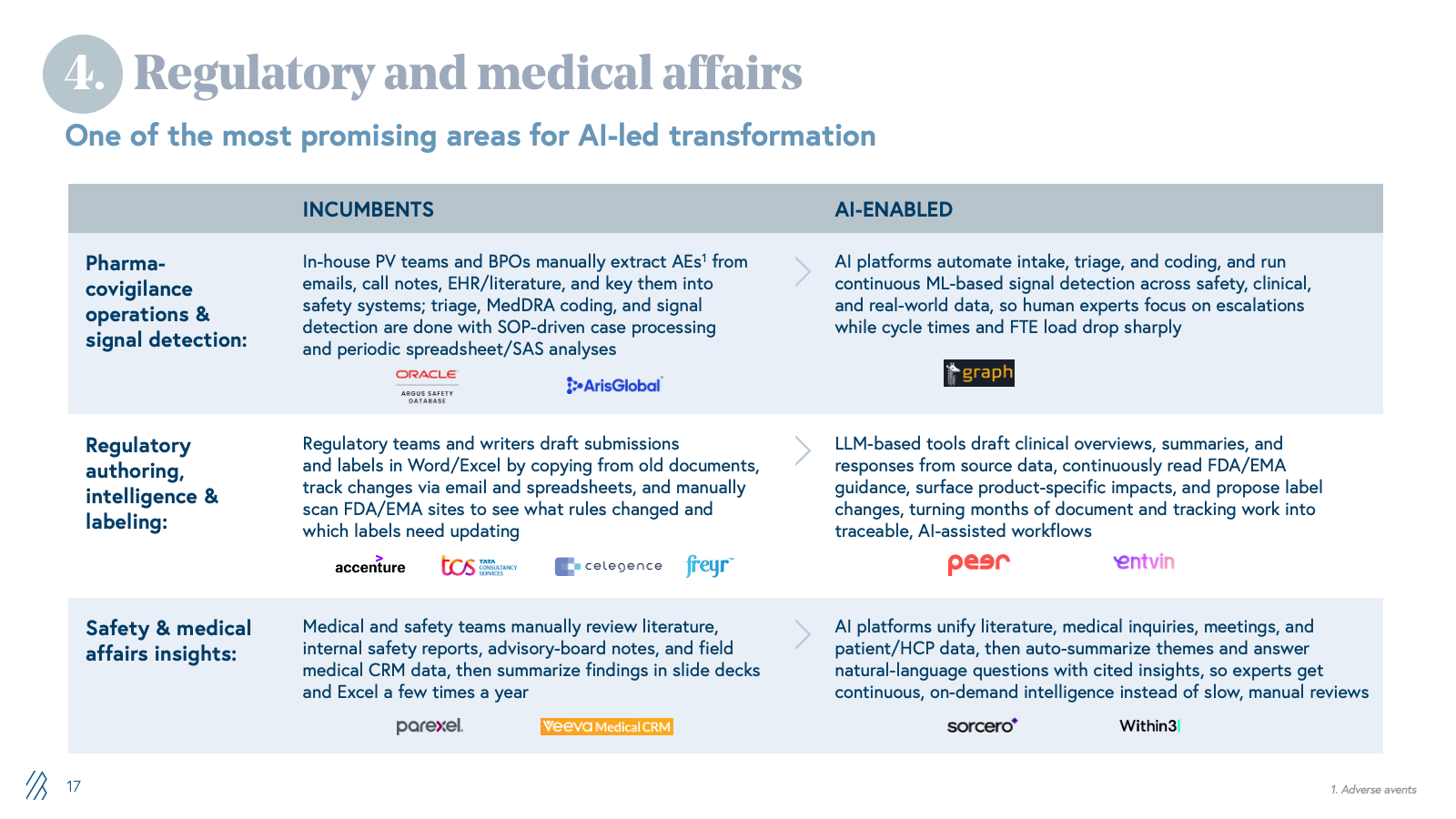

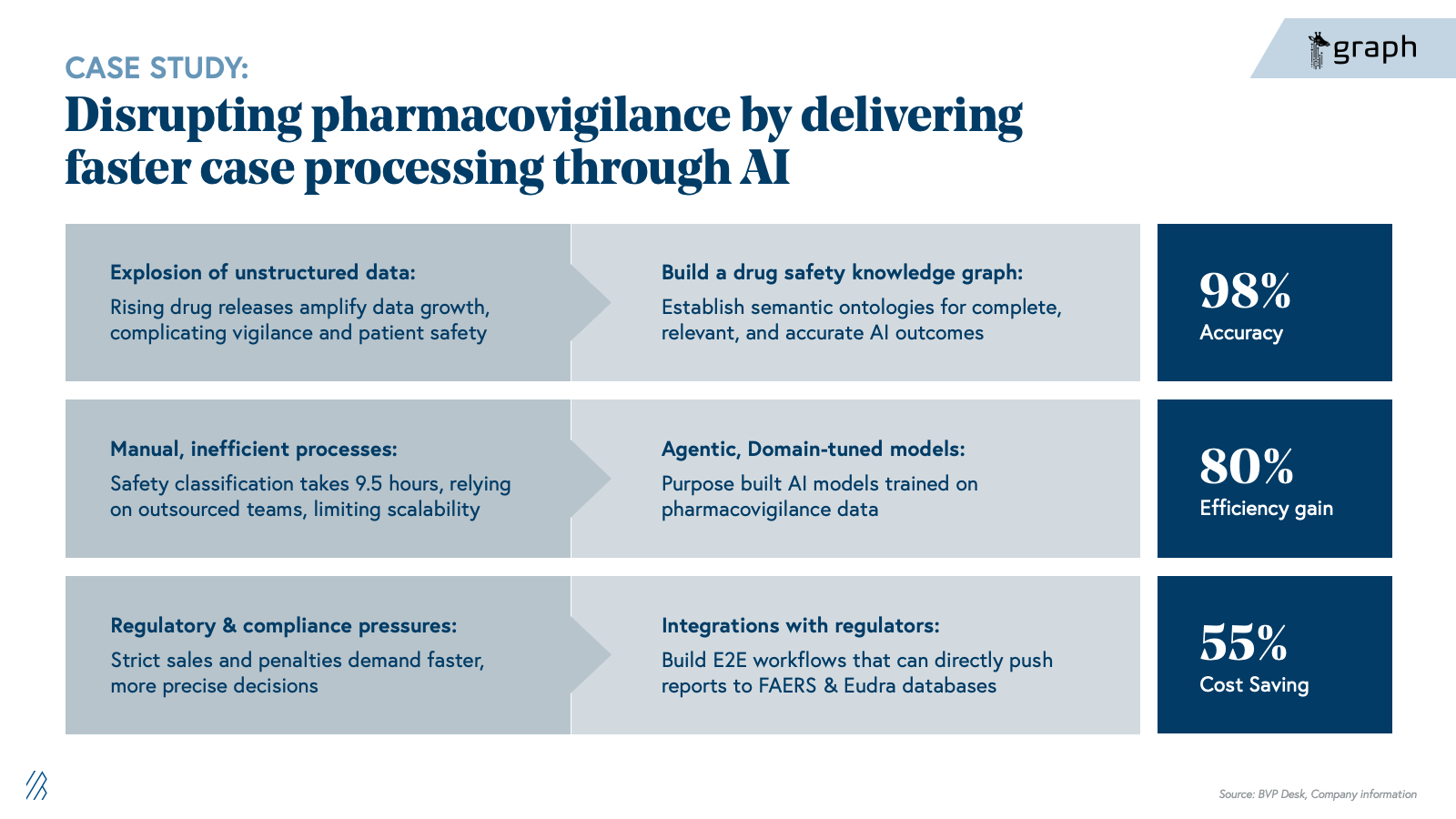

4. Regulatory and medical affairs

Pharma companies depend on specialized LS vendors and IT/BPO firms for submission preparation, lifecycle maintenance, pharmacovigilance case processing, signal detection, and medical writing. These workflows are manual, heavily documented, and run through fragmented safety databases, content management systems, and shared drives. Margins depend on case-processing volume and headcount.

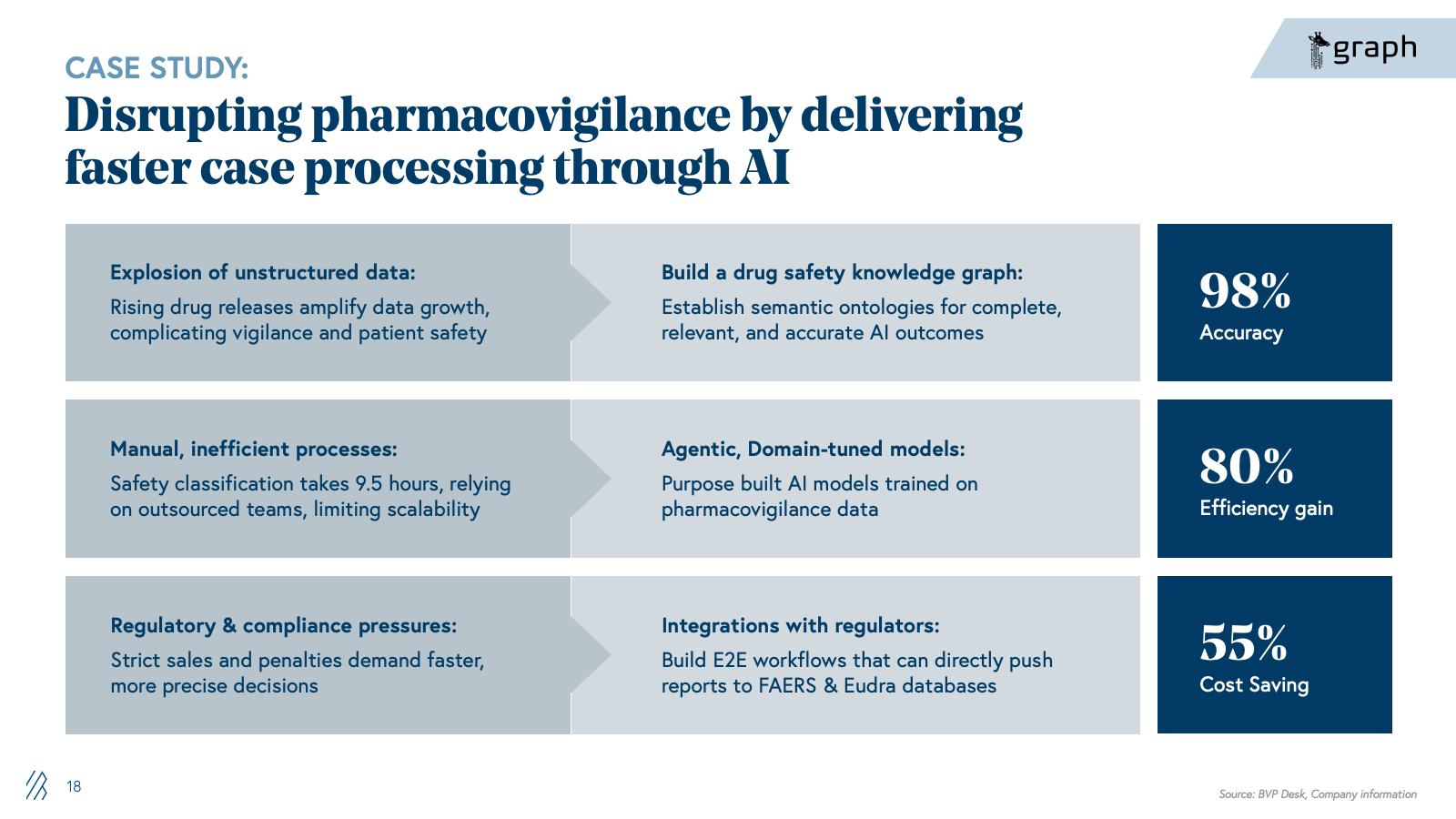

With AI, companies can now automate the knowledge work that dominates regulatory and safety operations. Case triage and MedDRA coding shift from manual, SOP-driven processing to AI-powered classification and anomaly detection. Signal detection moves from labor-intensive manual review across fragmented safety databases to continuous, context-aware monitoring across structured and unstructured data sources. Regulatory authoring shifts from manual drafting in Word to LLM-assisted generation of submissions and labeling updates. Medical affairs intelligence transitions from manual literature review to continuous AI-driven synthesis of safety signals, clinical evidence, and patient insights.

The advent of life sciences–optimized foundation models is also accelerating this shift. Anthropic's Claude for Life Sciences offers connectors to platforms like PubMed, Benchling, BioRender, and 10x Genomics, along with agent skills and a dedicated prompt library, enabling researchers to streamline literature reviews, bioinformatics analysis, protocol generation, and first-draft regulatory writing that previously required more manual effort and custom integration. At the same time, these platforms still aren’t full PV or regulatory systems; they don’t natively handle safety databases, MedDRA/WHO-DD, E2B, or validated signal detection, which means they act as an enabling infrastructure layer rather than a direct replacement for specialist vendors. The real opportunity for startups is to build on top of these models, not compete with them: winners will encode end-to-end regulatory and safety workflows, proprietary data integrations, and GxP-grade auditability, while “thin” LLM wrappers around public data and generic summarization will be quickly commoditized.

The shift is existential for BPOs built on case-processing volume and LS specialist firms charging for manual expertise. Our view is that the winners will not be generic LLM toolkits, but providers that deeply understand regulatory and safety nuances, can demonstrate auditability, and can sit comfortably in front of regulators and quality organizations.

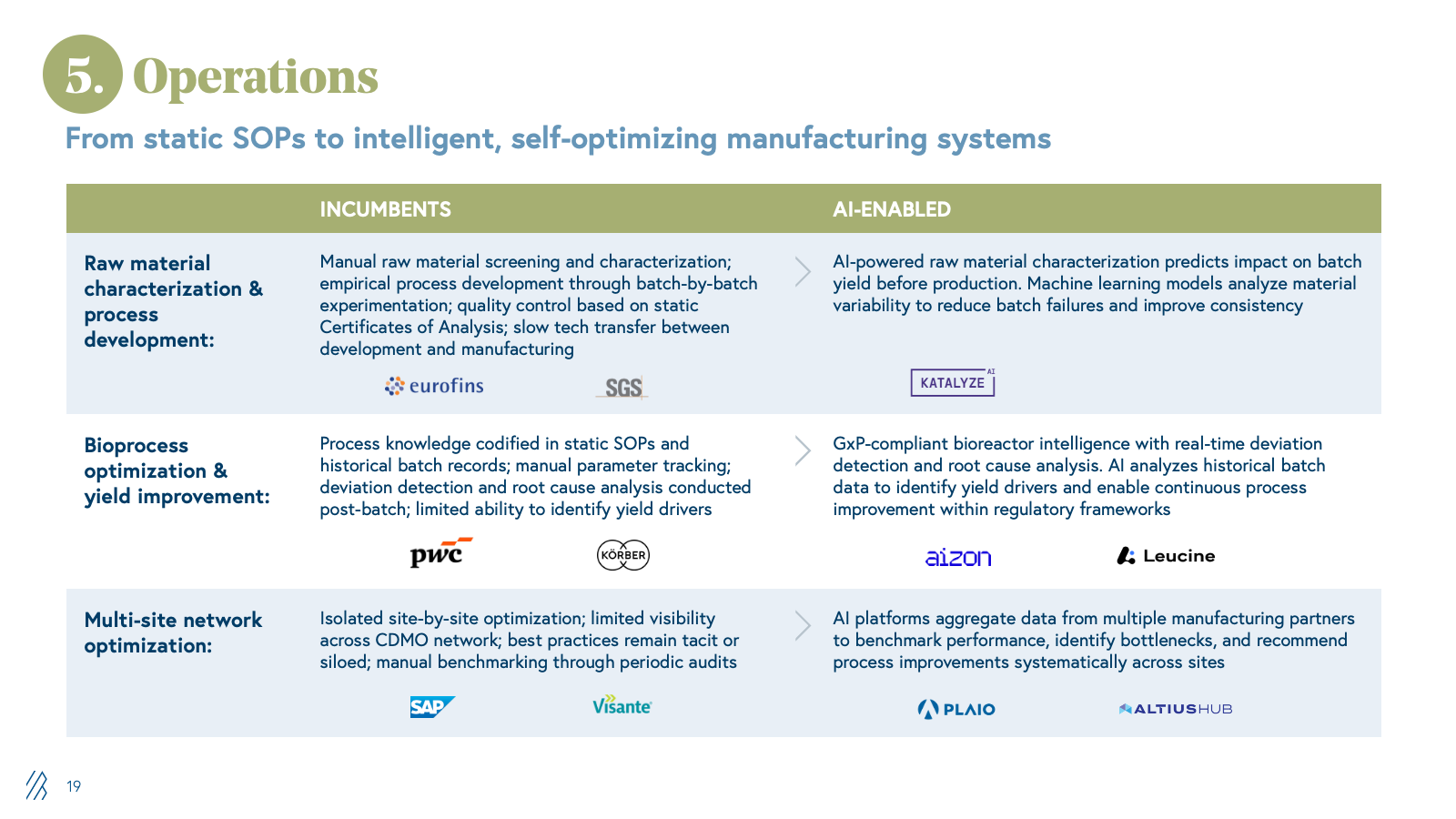

5. Manufacturing operations

The pharmaceutical industry relies on a broad ecosystem of partners to optimize manufacturing and supply chain operations, such as process consulting firms, supply chain analytics vendors, quality and compliance software providers, and specialized engineering firms. These partners help CDMOs and CMOs improve yields, reduce waste, accelerate tech transfer, and optimize procurement, which means:

- Margins depend on consulting hours, software licensing, and project-based engagements

- Process optimization and supply chain visibility remain largely manual, fragmented across disparate systems.

The value AI unlocks is converting unstructured manufacturing data into actionable intelligence. Raw material characterization and process development are accelerated by predicting the impact on batch yield before production, eliminating months of experimental iteration. Bioprocess optimization moves from static SOP compliance to real-time deviation detection and continuous improvement. Multi-site network optimization aggregates data across manufacturing partners to identify bottlenecks and systematize performance improvements.

For traditional consulting and software vendors in this space, AI creates existential pressure. When pharma companies and CDMOs can access AI-powered yield optimization, supply chain visibility, and process intelligence in real time, the need for retained consulting engagements and periodic optimization projects collapses. Providers who embed AI into manufacturing operations, delivering measurable yield and cost improvements, will capture share from consultancies and vendors whose value proposition depends on labor-intensive analysis and manual recommendations.

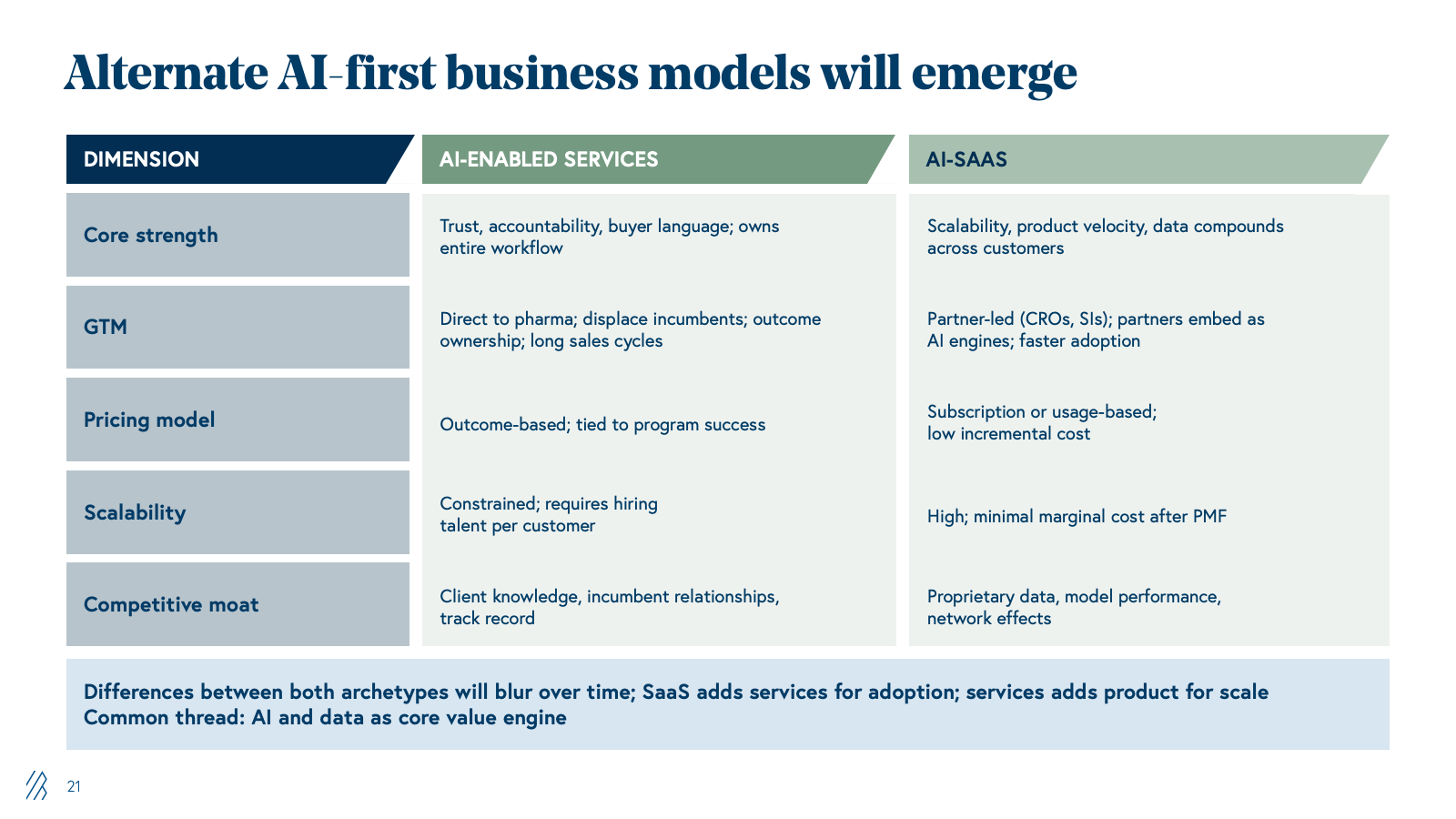

Two types of AI-first challengers

Across all of these value chains, two AI‑first archetypes are emerging.

AI-integrated services firms

These firms lead with domain experts wrapped in proprietary platforms for clinical trial design, regulatory submissions, or commercial analytics. They can sell directly to pharma because they speak the buyer’s language, take end-to-end responsibility for outcomes, and plug into familiar services budgets. For example, a leader of clinical operations is used to hiring a CRO or consulting firm to “own” an indication or program, and if that vendor is delivering through AI-powered tools rather than spreadsheets, the results are better. Once they prove they can, for example, redesign protocols to cut sites or shorten enrollment, land-and-expand becomes powerful. These vendors can move from one function to adjacent ones (e.g., clinical into safety, safety into regulatory) inside the same account.

The real constraint is the go-to-market: sales cycles are long, and incumbents with deep client-specific knowledge are deeply entrenched, so winning net-new logos requires displacing trusted partners, not just winning on technology. Scaling still also depends on specialized talent and delivery capacity, so even with strong software leverage, growth requires building real operational muscle.

AI‑native SaaS challengers

By contrast, these SaaS challengers start from the other end- they build narrow, high‑leverage products for patient matching, trial feasibility, labeling updates, or next‑best‑action in commercial teams. Their advantage is scalability; once a product is built and validated, it can be rolled out across dozens of customers with minimal incremental cost and product velocity, since every customer’s data can make the model better (subject to privacy and governance).

However, it’s harder for them to go straight to pharma for mission‑critical workflows- a VP of development wants one accountable counterparty, not a patchwork of point tools. As a result, SaaS companies often go to market through services firms, such as CROs, specialist consultancies, and system integrators (SIs), who already own the relationship and can bundle the software into broader solutions. This partner-led motion can actually move quickly today, because most CROs and SIs don’t have deep AI capabilities of their own and are actively looking for “AI engines” to embed. But this also means sharing economics and influence, since the partner controls the customer relationship.

The net effect is that neither archetype is “better” in an absolute sense. AI‑integrated services win on trust, outcome ownership, and land‑and‑expand within big pharma; SaaS wins on scalability, margins, and product compounding. The most important pattern is that both are being pulled toward the middle- service firms becoming more productized, SaaS firms layering in services and integrations.

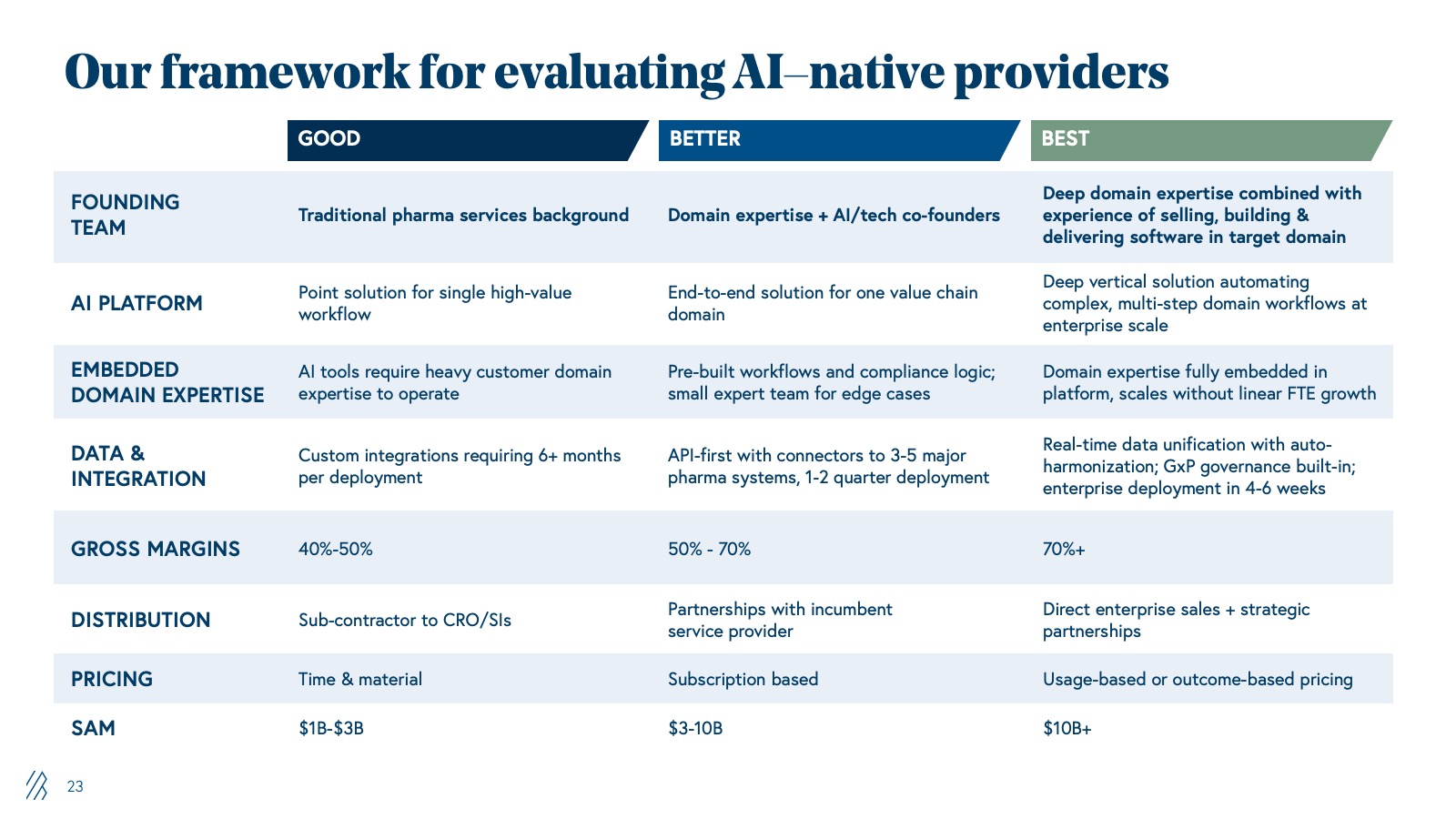

Our framework for evaluating AI-native providers

| Good | Better | Best | |

|

FOUNDING TEAM |

Traditional pharma services background |

Domain expertise + AI/tech co-founders |

Deep domain expertise combined with experience of selling, building, and delivering software in target domain |

|

AI PLATFORM |

Point solution for single high-value workflow |

End-to-end solution for one value chain domain |

Deep vertical solution automating complex, multi-step domain workflows at enterprise scale |

|

EMBEDDED DOMAIN EXPERTISE |

AI tools require heavy customer domain expertise to operate |

Pre-built workflows and compliance logic; small expert team for edge cases |

Domain expertise fully embedded in platform, scales without linear FTE growth |

|

DATA & INTEGRATION |

Custom integrations requiring 6+ months per deployment |

API-first with connectors to 3-5 major pharma systems, 1-2 quarter deployment |

Real-time data unification with auto-harmonization; GxP governance built-in; enterprise deployment in 4-6 weeks |

|

GROSS MARGINS |

40%-50% |

50% - 70% |

70%+ |

|

DISTRIBUTION |

Sub-contractor to CRO/SIs |

Partnerships with incumbent |

Direct enterprise sales + strategic partnerships |

|

PRICING |

Time & material |

Subscription based |

Usage-based or outcome-based pricing |

|

SAM |

$1B-$3B |

$3-10B |

$10B+ |

If you’re building in this space, we’d appreciate hearing from you. Reach out to us at india_ai@bvp.com